Confidence Intervals

This notebook overviews scalecast intervals, which are scored with Mean Scaled Interval Score (MSIS). Lower scores are better. This notebook requires scalecast>=0.18.0.

Scalecast uses a naive conformal interval, created from holding out a test-set of data and setting interval ranges from the percentiles of the test-set residuals. This simple approach allows every estimator type to get the same kind of interval. As we will see by scoring the intervals and comparing them to ARIMA intervals from statsmodels, the results are good.

To evaluate the intervals, we leave out a section of each series to score out-of-sample. This is usually not necessary for scalecast, as all models are tested automatically, but the confidence intervals can overfit on any test set stored in the Forecaster or MVForecaster object due to leakage that occurs when constructing these intervals. Scalecast intervals are compared to ARIMA intervals on the same series in the last section of this notebook and the scalecast intervals, on the whole,

perform better. The series used in this example are ordered from easiest-to-hardest to forecast.

Easy Distribution-Free Conformal Intervals for Time Series

[1]:

import pandas as pd

import numpy as np

from scalecast.Forecaster import Forecaster

from scalecast import GridGenerator

from scalecast.util import metrics

from scalecast.notebook import tune_test_forecast

from scalecast.SeriesTransformer import SeriesTransformer

import matplotlib.pyplot as plt

import seaborn as sns

import time

from tqdm.notebook import tqdm

[2]:

import warnings

warnings.simplefilter(action='ignore', category=DeprecationWarning)

[3]:

models = (

'mlr',

'elasticnet',

'ridge',

'knn',

'xgboost',

'lightgbm',

'gbt',

) # these are all scikit-learn models or APIs

# this will be used later to fill in results

results_template = pd.DataFrame(index=models)

[4]:

def score_cis(results, fcsts, ci_name, actuals, obs, val_len, models=models, m_=1):

for m in models:

results.loc[m,ci_name] = metrics.msis(

a = actuals,

uf = fcsts[m+'_upperci'],

lf = fcsts[m+'_lowerci'],

obs = obs,

m = m_,

)

return results

[5]:

GridGenerator.get_example_grids()

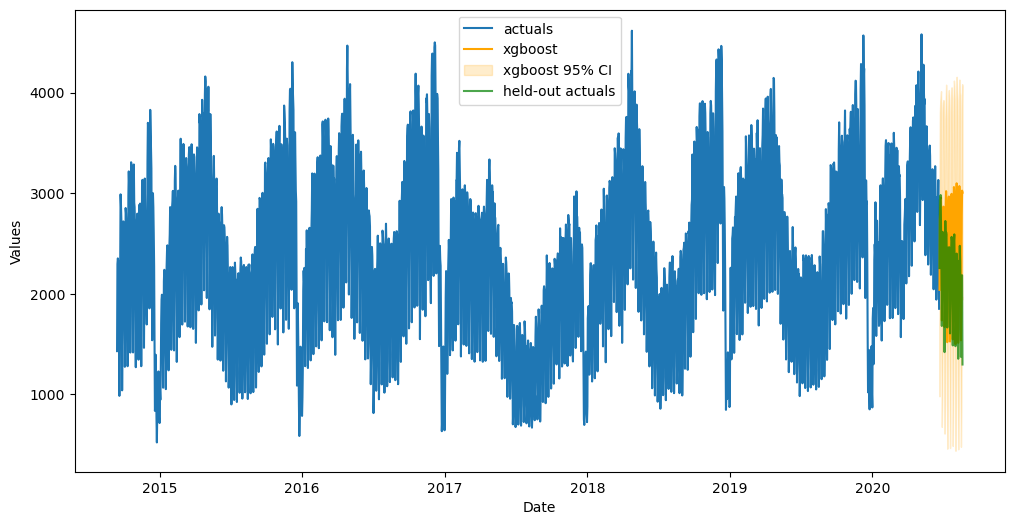

Daily Website Visitors

Link to data: https://www.kaggle.com/datasets/bobnau/daily-website-visitors

We will use a length of 180 observations (about half a year) both to tune and test the models

We want to optimize the forecasts and confidence intervals for a 60-day forecast horizon

[6]:

val_len = 180

fcst_len = 60

[7]:

data = pd.read_csv('daily-website-visitors.csv',parse_dates=['Date']).set_index('Date')

data.head()

[7]:

| Row | Day | Day.Of.Week | Page.Loads | Unique.Visits | First.Time.Visits | Returning.Visits | |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 2014-09-14 | 1 | Sunday | 1 | 2,146 | 1,582 | 1430 | 152 |

| 2014-09-15 | 2 | Monday | 2 | 3,621 | 2,528 | 2297 | 231 |

| 2014-09-16 | 3 | Tuesday | 3 | 3,698 | 2,630 | 2352 | 278 |

| 2014-09-17 | 4 | Wednesday | 4 | 3,667 | 2,614 | 2327 | 287 |

| 2014-09-18 | 5 | Thursday | 5 | 3,316 | 2,366 | 2130 | 236 |

[8]:

visits_sep = data['First.Time.Visits'].iloc[-fcst_len:]

visits = data['First.Time.Visits'].iloc[:-fcst_len]

[9]:

f=Forecaster(

y=visits,

current_dates=visits.index,

future_dates=fcst_len,

test_length = val_len,

validation_length = val_len, # for hyperparameter tuning

cis = True, # set to True at initialization to always evaluate cis

)

f.auto_Xvar_select(

estimator='elasticnet',

alpha=.2,

max_ar=100,

monitor='ValidationMetricValue',

)

f

[9]:

Forecaster(

DateStartActuals=2014-09-14T00:00:00.000000000

DateEndActuals=2020-06-20T00:00:00.000000000

Freq=D

N_actuals=2107

ForecastLength=60

Xvars=['t', 'AR1', 'AR2', 'AR3', 'AR4', 'AR5', 'AR6', 'AR7', 'AR8', 'AR9', 'AR10', 'AR11', 'AR12', 'AR13', 'AR14', 'AR15', 'AR16', 'AR17', 'AR18', 'AR19', 'AR20', 'AR21', 'AR22', 'AR23', 'AR24', 'AR25', 'AR26', 'AR27', 'AR28', 'AR29', 'AR30', 'AR31', 'AR32', 'AR33', 'AR34', 'AR35', 'AR36', 'AR37', 'AR38', 'AR39', 'AR40', 'AR41', 'AR42', 'AR43', 'AR44', 'AR45', 'AR46', 'AR47', 'AR48', 'AR49', 'AR50', 'AR51', 'AR52', 'AR53', 'AR54', 'AR55', 'AR56', 'AR57', 'AR58', 'AR59', 'AR60', 'AR61', 'AR62', 'AR63', 'AR64', 'AR65', 'AR66', 'AR67', 'AR68', 'AR69', 'AR70', 'AR71', 'AR72', 'AR73', 'AR74', 'AR75', 'AR76', 'AR77', 'AR78', 'AR79', 'AR80', 'AR81', 'AR82', 'AR83', 'AR84', 'AR85', 'AR86', 'AR87', 'AR88', 'AR89', 'AR90', 'AR91', 'AR92', 'AR93', 'AR94', 'AR95', 'AR96', 'AR97', 'AR98', 'AR99', 'AR100']

TestLength=180

ValidationMetric=rmse

ForecastsEvaluated=[]

CILevel=0.95

CurrentEstimator=mlr

GridsFile=Grids

)

[10]:

tune_test_forecast(

f,

models,

)

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

[11]:

ms = f.export('model_summaries',determine_best_by='TestSetRMSE')

ms[['ModelNickname','TestSetRMSE','InSampleRMSE']]

[11]:

| ModelNickname | TestSetRMSE | InSampleRMSE | |

|---|---|---|---|

| 0 | xgboost | 532.374846 | 14.496801 |

| 1 | lightgbm | 582.261645 | 112.543232 |

| 2 | knn | 788.704950 | 306.828988 |

| 3 | elasticnet | 794.649818 | 186.616620 |

| 4 | ridge | 798.711718 | 187.026325 |

| 5 | mlr | 803.931314 | 185.620629 |

| 6 | gbt | 1171.782785 | 147.478748 |

We will demonstrate how the confidence intervals change as they are re-evaluated using the best model according to the test RMSE.

Evaluate Interval

[12]:

fig, ax = plt.subplots(figsize=(12,6))

f.plot(ci=True,models='top_1',order_by='TestSetRMSE',ax=ax)

sns.lineplot(

y = 'First.Time.Visits',

x = 'Date',

data = visits_sep.reset_index(),

ax = ax,

label = 'held-out actuals',

color = 'green',

alpha = 0.7,

)

plt.show()

[13]:

# export test-set preds and confidence intervals

fcsts1 = f.export("lvl_fcsts",cis=True)

fcsts1.head()

[13]:

| DATE | mlr | mlr_upperci | mlr_lowerci | elasticnet | elasticnet_upperci | elasticnet_lowerci | ridge | ridge_upperci | ridge_lowerci | ... | knn_lowerci | xgboost | xgboost_upperci | xgboost_lowerci | lightgbm | lightgbm_upperci | lightgbm_lowerci | gbt | gbt_upperci | gbt_lowerci | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2020-06-21 | 2190.555279 | 3464.907755 | 916.202804 | 2194.962019 | 3452.970789 | 936.953250 | 2191.868075 | 3464.239858 | 919.496293 | ... | 812.176316 | 2039.648438 | 3098.496887 | 980.799988 | 2198.858468 | 3232.664729 | 1165.052207 | 2125.968510 | 4021.476092 | 230.460929 |

| 1 | 2020-06-22 | 2835.674158 | 4110.026633 | 1561.321683 | 2823.011263 | 4081.020033 | 1565.002493 | 2831.886812 | 4104.258594 | 1559.515029 | ... | 1612.281579 | 2743.368896 | 3802.217346 | 1684.520447 | 2820.575637 | 3854.381898 | 1786.769376 | 2729.050006 | 4624.557587 | 833.542425 |

| 2 | 2020-06-23 | 2975.510723 | 4249.863198 | 1701.158248 | 2944.846465 | 4202.855235 | 1686.837696 | 2972.183687 | 4244.555469 | 1699.811904 | ... | 1804.176316 | 2851.803711 | 3910.652161 | 1792.955261 | 2819.654176 | 3853.460437 | 1785.847915 | 2880.262061 | 4775.769642 | 984.754480 |

| 3 | 2020-06-24 | 3038.258157 | 4312.610632 | 1763.905681 | 3006.932564 | 4264.941333 | 1748.923794 | 3033.992818 | 4306.364600 | 1761.621035 | ... | 1673.860526 | 2905.132568 | 3963.981018 | 1846.284119 | 2824.992206 | 3858.798467 | 1791.185945 | 2930.293895 | 4825.801476 | 1034.786314 |

| 4 | 2020-06-25 | 3032.580568 | 4306.933043 | 1758.228093 | 3011.122478 | 4269.131247 | 1753.113708 | 3021.274091 | 4293.645873 | 1748.902309 | ... | 1475.386842 | 2955.912598 | 4014.761047 | 1897.064148 | 2961.588543 | 3995.394805 | 1927.782282 | 3029.007375 | 4924.514956 | 1133.499794 |

5 rows × 22 columns

The values in the below table are mean scaled interval scores for confidence intervals. Lower scores are better.

[14]:

results = score_cis(

results_template.copy(),

fcsts1,

'Daily Visitors',

visits_sep,

visits,

val_len = val_len,

)

results

[14]:

| Daily Visitors | |

|---|---|

| mlr | 5.632456 |

| elasticnet | 5.548336 |

| ridge | 5.622506 |

| knn | 5.639715 |

| xgboost | 5.597762 |

| lightgbm | 5.196714 |

| gbt | 8.319963 |

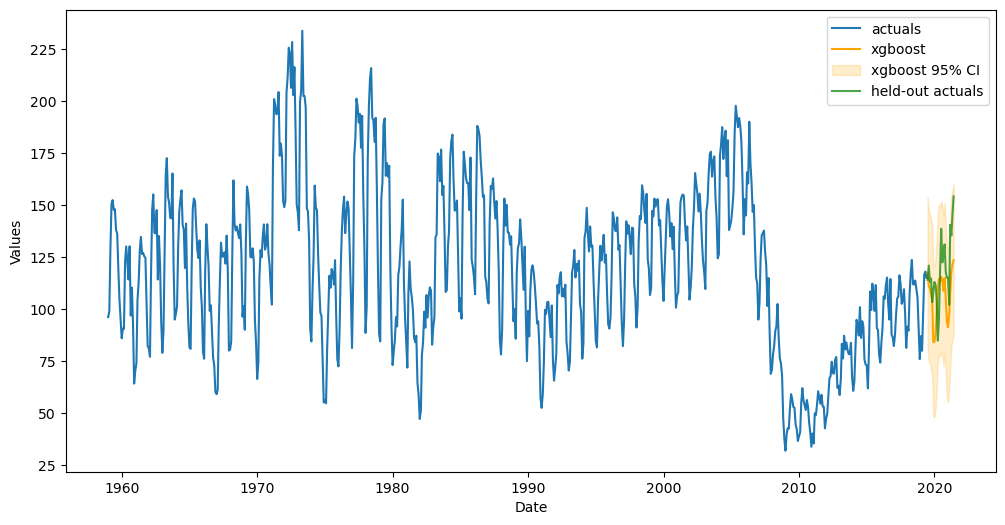

Housing Starts

Link to data: https://fred.stlouisfed.org/series/HOUSTNSA

We will use a length of 96 observations (8 years) both to tune and test the models

We want to optimize the forecasts and confidence intervals for a 24-month forecast horizon

[15]:

import pandas_datareader as pdr

[16]:

val_len = 96

fcst_len = 24

[17]:

housing = pdr.get_data_fred('HOUSTNSA',start='1900-01-01',end='2021-06-01')

housing.head()

[17]:

| HOUSTNSA | |

|---|---|

| DATE | |

| 1959-01-01 | 96.2 |

| 1959-02-01 | 99.0 |

| 1959-03-01 | 127.7 |

| 1959-04-01 | 150.8 |

| 1959-05-01 | 152.5 |

[18]:

starts_sep = housing.iloc[-fcst_len:,0]

starts = housing.iloc[:-fcst_len,0]

[19]:

f = Forecaster(

y=starts,

current_dates=starts.index,

future_dates=fcst_len,

test_length=val_len,

validation_length=val_len,

cis=True,

)

# difference the data for stationary modeling

transformer = SeriesTransformer(f)

f = transformer.DiffTransform(1)

# find best xvars to forecast with

f.auto_Xvar_select(

estimator='elasticnet',

alpha=.2,

max_ar=100,

monitor='ValidationMetricValue', # not test set

)

f

[19]:

Forecaster(

DateStartActuals=1959-02-01T00:00:00.000000000

DateEndActuals=2019-06-01T00:00:00.000000000

Freq=MS

N_actuals=725

ForecastLength=24

Xvars=['monthsin', 'monthcos', 'quartersin', 'quartercos', 'AR1', 'AR2', 'AR3', 'AR4', 'AR5', 'AR6', 'AR7', 'AR8', 'AR9', 'AR10', 'AR11', 'AR12', 'AR13', 'AR14', 'AR15', 'AR16', 'AR17', 'AR18', 'AR19', 'AR20', 'AR21', 'AR22', 'AR23', 'AR24', 'AR25', 'AR26', 'AR27', 'AR28', 'AR29', 'AR30', 'AR31', 'AR32', 'AR33', 'AR34', 'AR35', 'AR36', 'AR37', 'AR38', 'AR39', 'AR40', 'AR41', 'AR42', 'AR43', 'AR44', 'AR45', 'AR46', 'AR47', 'AR48', 'AR49', 'AR50', 'AR51', 'AR52', 'AR53', 'AR54', 'AR55', 'AR56', 'AR57', 'AR58', 'AR59', 'AR60', 'AR61', 'AR62', 'AR63', 'AR64', 'AR65', 'AR66', 'AR67', 'AR68', 'AR69', 'AR70', 'AR71', 'AR72', 'AR73', 'AR74', 'AR75', 'AR76', 'AR77', 'AR78', 'AR79', 'AR80', 'AR81', 'AR82', 'AR83', 'AR84', 'AR85', 'AR86', 'AR87', 'AR88', 'AR89', 'AR90', 'AR91', 'AR92', 'AR93', 'AR94', 'AR95', 'AR96', 'AR97', 'AR98', 'AR99', 'AR100']

TestLength=96

ValidationMetric=rmse

ForecastsEvaluated=[]

CILevel=0.95

CurrentEstimator=mlr

GridsFile=Grids

)

[20]:

tune_test_forecast(

f,

models,

dynamic_testing = fcst_len,

)

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

[21]:

# rever the difftransform

f = transformer.DiffRevert(1)

[22]:

ms = f.export('model_summaries',determine_best_by='TestSetRMSE')

ms[['ModelNickname','TestSetRMSE','InSampleRMSE']]

[22]:

| ModelNickname | TestSetRMSE | InSampleRMSE | |

|---|---|---|---|

| 0 | xgboost | 21.402469 | 3.112793 |

| 1 | lightgbm | 23.160361 | 27.660879 |

| 2 | mlr | 30.059747 | 71.624715 |

| 3 | gbt | 38.185841 | 38.657789 |

| 4 | knn | 42.432505 | 146.502991 |

| 5 | ridge | 46.457215 | 55.969584 |

| 6 | elasticnet | 53.111686 | 38.237499 |

Evaluate Interval

[23]:

fig, ax = plt.subplots(figsize=(12,6))

f.plot(ci=True,models='top_1',order_by='TestSetRMSE',ax=ax)

sns.lineplot(

y = 'HOUSTNSA',

x = 'DATE',

data = starts_sep.reset_index(),

ax = ax,

label = 'held-out actuals',

color = 'green',

alpha = 0.7,

)

plt.show()

[24]:

housing_fcsts1 = f.export("lvl_fcsts",cis=True)

housing_results = score_cis(

results_template.copy(),

housing_fcsts1,

'Housing Starts',

starts_sep,

starts,

val_len = val_len,

m_ = 12, # monthly seasonality

)

housing_results

[24]:

| Housing Starts | |

|---|---|

| mlr | 5.661675 |

| elasticnet | 8.247183 |

| ridge | 7.432564 |

| knn | 6.552641 |

| xgboost | 3.930183 |

| lightgbm | 4.289493 |

| gbt | 5.884677 |

[25]:

results['Housing Starts'] = housing_results['Housing Starts']

results

[25]:

| Daily Visitors | Housing Starts | |

|---|---|---|

| mlr | 5.632456 | 5.661675 |

| elasticnet | 5.548336 | 8.247183 |

| ridge | 5.622506 | 7.432564 |

| knn | 5.639715 | 6.552641 |

| xgboost | 5.597762 | 3.930183 |

| lightgbm | 5.196714 | 4.289493 |

| gbt | 8.319963 | 5.884677 |

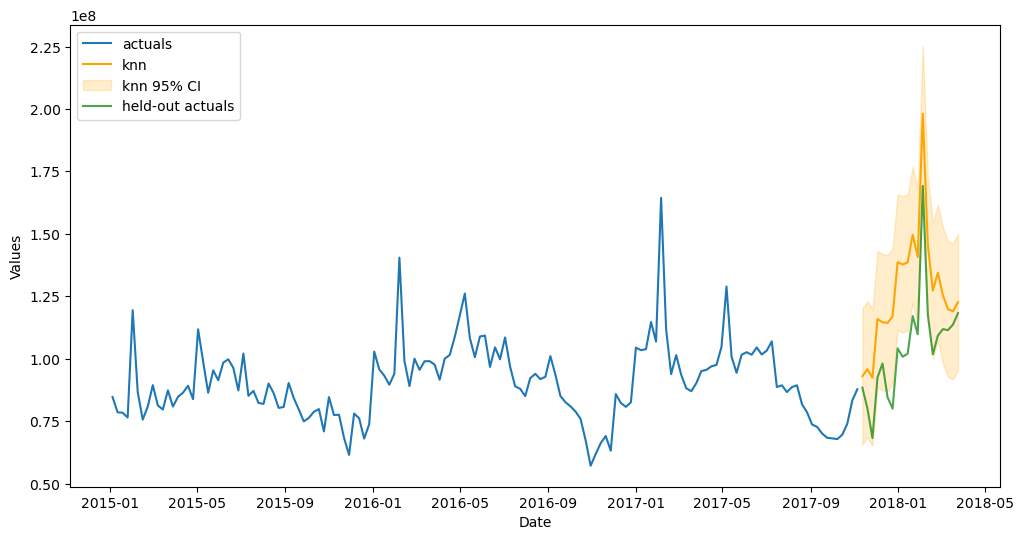

Avocado Sales

Link to data: https://www.kaggle.com/datasets/neuromusic/avocado-prices

We will use a length of 20 observations both to tune and test the models (95% CIs require at least 20 observations in the test set)

We want to optimize the forecasts and confidence intervals for a 20-week forecast horizon

[26]:

# change display settings

pd.options.display.float_format = '{:,.2f}'.format

[27]:

val_len = 20

fcst_len = 20

[28]:

avocados = pd.read_csv('avocado.csv',parse_dates = ['Date'])

volume = avocados.groupby('Date')['Total Volume'].sum()

[29]:

volume.reset_index().head()

[29]:

| Date | Total Volume | |

|---|---|---|

| 0 | 2015-01-04 | 84,674,337.20 |

| 1 | 2015-01-11 | 78,555,807.24 |

| 2 | 2015-01-18 | 78,388,784.08 |

| 3 | 2015-01-25 | 76,466,281.07 |

| 4 | 2015-02-01 | 119,453,235.25 |

[30]:

volume_sep = volume.iloc[-fcst_len:]

volume = volume.iloc[:-fcst_len]

[31]:

f = Forecaster(

y = volume,

current_dates = volume.index,

future_dates = fcst_len,

test_length = val_len,

validation_length = val_len,

cis = True,

)

# difference the data for stationary modeling

transformer = SeriesTransformer(f)

f = transformer.DiffTransform(1)

f = transformer.DiffTransform(52) # seasonal differencing

# find best xvars

f.auto_Xvar_select(

estimator='elasticnet',

alpha=.2,

max_ar=26,

monitor='ValidationMetricValue', # not test set

decomp_trend=False,

)

f

[31]:

Forecaster(

DateStartActuals=2016-01-10T00:00:00.000000000

DateEndActuals=2017-11-05T00:00:00.000000000

Freq=W-SUN

N_actuals=96

ForecastLength=20

Xvars=['weeksin', 'weekcos', 'AR1', 'AR2', 'AR3', 'AR4', 'AR5', 'AR6', 'AR7', 'AR8', 'AR9']

TestLength=20

ValidationMetric=rmse

ForecastsEvaluated=[]

CILevel=0.95

CurrentEstimator=mlr

GridsFile=Grids

)

[32]:

tune_test_forecast(

f,

models,

dynamic_testing = fcst_len,

)

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

[33]:

# revert differencing

f = transformer.DiffRevert(52)

f = transformer.DiffRevert(1)

[34]:

ms = f.export('model_summaries',determine_best_by='TestSetRMSE')

ms[['ModelNickname','TestSetRMSE','InSampleRMSE']]

[34]:

| ModelNickname | TestSetRMSE | InSampleRMSE | |

|---|---|---|---|

| 0 | knn | 12,792,100.70 | 14,090,078.03 |

| 1 | ridge | 13,457,205.75 | 23,224,298.55 |

| 2 | elasticnet | 13,532,378.91 | 23,130,014.21 |

| 3 | mlr | 13,532,379.31 | 23,130,012.59 |

| 4 | lightgbm | 15,265,692.24 | 21,365,608.04 |

| 5 | gbt | 20,539,987.16 | 18,023,127.21 |

| 6 | xgboost | 21,487,561.26 | 12,876.01 |

Evaluate Interval

[35]:

fig, ax = plt.subplots(figsize=(12,6))

f.plot(ci=True,models='top_1',order_by='TestSetRMSE',ax=ax)

sns.lineplot(

y = 'Total Volume',

x = 'Date',

data = volume_sep.reset_index(),

ax = ax,

label = 'held-out actuals',

color = 'green',

alpha = 0.7,

)

plt.show()

[36]:

avc_fcsts1 = f.export("lvl_fcsts",cis=True)

avc_results = score_cis(

results_template.copy(),

avc_fcsts1,

'Avocados',

volume_sep,

volume,

val_len = val_len,

models = models,

)

avc_results

[36]:

| Avocados | |

|---|---|

| mlr | 8.55 |

| elasticnet | 8.55 |

| ridge | 8.48 |

| knn | 19.70 |

| xgboost | 13.74 |

| lightgbm | 19.81 |

| gbt | 10.65 |

[37]:

results['Avocados'] = avc_results['Avocados']

results

[37]:

| Daily Visitors | Housing Starts | Avocados | |

|---|---|---|---|

| mlr | 5.63 | 5.66 | 8.55 |

| elasticnet | 5.55 | 8.25 | 8.55 |

| ridge | 5.62 | 7.43 | 8.48 |

| knn | 5.64 | 6.55 | 19.70 |

| xgboost | 5.60 | 3.93 | 13.74 |

| lightgbm | 5.20 | 4.29 | 19.81 |

| gbt | 8.32 | 5.88 | 10.65 |

All Aggregated Results

[38]:

_, ax = plt.subplots(figsize=(12,6))

sns.heatmap(

results,

annot=True,

fmt='.2f',

cmap="Spectral_r",

ax=ax

)

plt.show()

For the most part, the linear models set the best intervals and the boosted tree models were very good or very bad, with GBT more towards the bad side.

Benchmark Against StatsModels ARIMA

Confidence intervals come from StatsModels but the auto-ARIMA process is from PMDARIMA.

[39]:

from scalecast.auxmodels import auto_arima

[40]:

all_series = {

# series,out-of-sample series,seasonal step

'visitors':[visits,visits_sep,1],

'housing starts':[starts,starts_sep,12],

'avocados':[volume,volume_sep,1]

}

arima_conformal_results = pd.DataFrame()

arima_sm_results = pd.DataFrame()

[41]:

for k, v in all_series.items():

print(k)

f = Forecaster(

y=v[0],

current_dates=v[0].index,

future_dates=len(v[1]),

test_length = len(v[1]),

cis=True,

)

auto_arima(f,m=v[2])

arima_results = f.export("lvl_fcsts",cis=True)

# scalecast intervals

arima_conformal_results.loc[k,'MSIS'] = metrics.msis(

a = v[1].values,

uf = arima_results['auto_arima_upperci'].values,

lf = arima_results['auto_arima_lowerci'].values,

obs = v[0].values,

m = v[2],

)

# statsmodels intervals

cis = f.regr.get_forecast(len(v[1])).conf_int()

arima_sm_results.loc[k,'MSIS'] = metrics.msis(

a = v[1].values,

uf = cis.T[1],

lf = cis.T[0],

obs = v[0].values,

m = v[2],

)

visitors

housing starts

avocados

MSIS Results - ARIMA Scalecast

[42]:

# results from the scalecast intervals

arima_conformal_results

[42]:

| MSIS | |

|---|---|

| visitors | 4.97 |

| housing starts | 24.90 |

| avocados | 23.15 |

[43]:

arima_conformal_results.mean()

[43]:

MSIS 17.67

dtype: float64

MSIS Results - ARIMA StatsModels

[44]:

# results from the statsmodels intervals

arima_sm_results

[44]:

| MSIS | |

|---|---|

| visitors | 5.80 |

| housing starts | 5.62 |

| avocados | 19.94 |

[45]:

arima_sm_results.mean()

[45]:

MSIS 10.46

dtype: float64

[46]:

all_results = results.copy()

all_results.loc['arima (conformal)'] = arima_conformal_results.T.values[0]

all_results.loc['arima (statsmodels) - benchmark'] = arima_sm_results.T.values[0]

all_results = all_results.T

all_results

[46]:

| mlr | elasticnet | ridge | knn | xgboost | lightgbm | gbt | arima (conformal) | arima (statsmodels) - benchmark | |

|---|---|---|---|---|---|---|---|---|---|

| Daily Visitors | 5.63 | 5.55 | 5.62 | 5.64 | 5.60 | 5.20 | 8.32 | 4.97 | 5.80 |

| Housing Starts | 5.66 | 8.25 | 7.43 | 6.55 | 3.93 | 4.29 | 5.88 | 24.90 | 5.62 |

| Avocados | 8.55 | 8.55 | 8.48 | 19.70 | 13.74 | 19.81 | 10.65 | 23.15 | 19.94 |

[47]:

def highlight_rows(row):

ret_row = ['']*all_results.shape[1]

for i, c in enumerate(all_results.iloc[:,:-1]):

if row[c] < row['arima (statsmodels) - benchmark']:

ret_row[i] = 'background-color: lightgreen;'

else:

ret_row[i] = 'background-color: lightcoral;'

return ret_row

all_results.style.apply(

highlight_rows,

axis=1,

)

[47]:

| mlr | elasticnet | ridge | knn | xgboost | lightgbm | gbt | arima (conformal) | arima (statsmodels) - benchmark | |

|---|---|---|---|---|---|---|---|---|---|

| Daily Visitors | 5.632456 | 5.548336 | 5.622506 | 5.639715 | 5.597762 | 5.196714 | 8.319963 | 4.966161 | 5.796559 |

| Housing Starts | 5.661675 | 8.247183 | 7.432564 | 6.552641 | 3.930183 | 4.289493 | 5.884677 | 24.897373 | 5.624803 |

| Avocados | 8.551783 | 8.551783 | 8.478400 | 19.700378 | 13.743804 | 19.810258 | 10.654140 | 23.151315 | 19.944485 |

The above table shows which scalecast intervals performed better or worse than the ARIMA interval. Green scores are better, red are worse. The scalecast conformal intervals were on the whole better, but not always. When comparing ARIMA to ARIMA, the confidence intervals from statsmodels performed slightly worse on one series, slightly better on another, and significantly better on the remaining one. The rest of the models run through scalecast usually beat the ARIMA intervals on all datasets, except housing starts. XGBoost and Lightgbm were the only models to always beat the intervals from StatsModels. On the whole, the scalecast interval has a nice showing against the more traditional interval from ARIMA in the StatsModels package.

[ ]: