Introductory Example

This demonstrates an example using scalecast 0.18.0. Several features explored are not available in earlier versions, so if anything is not working, try upgrading:

pip install --upgrade scalecast

If things are still not working, you spot a typo, or you have some other suggestion to improve functionality or document readability, open an issue or email mikekeith52@gmail.com.

Link to dataset used in this example: https://www.kaggle.com/datasets/neuromusic/avocado-prices.

Latest official documentation.

[1]:

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

[2]:

# read in data

data = pd.read_csv('avocado.csv',parse_dates = ['Date'])

data = data.sort_values(['region','type','Date'])

Univariate Forecasting

Load the Forecaster Object

This is an object that can store data, run forecasts, store results, and plot. It’s a UI, procedure, and set of models all-in-one.

Forecasts in scalecast are run with a dynamic recursive approach by default, as opposed to a direct or other approach.

[3]:

from scalecast.Forecaster import Forecaster

[4]:

volume = data.groupby('Date')['Total Volume'].sum()

[5]:

f = Forecaster(

y = volume,

current_dates = volume.index,

future_dates = 13,

)

f

[5]:

Forecaster(

DateStartActuals=2015-01-04T00:00:00.000000000

DateEndActuals=2018-03-25T00:00:00.000000000

Freq=W-SUN

N_actuals=169

ForecastLength=13

Xvars=[]

TestLength=0

ValidationMetric=rmse

ForecastsEvaluated=[]

CILevel=None

CurrentEstimator=mlr

GridsFile=Grids

)

Exploratory Data Analysis

[6]:

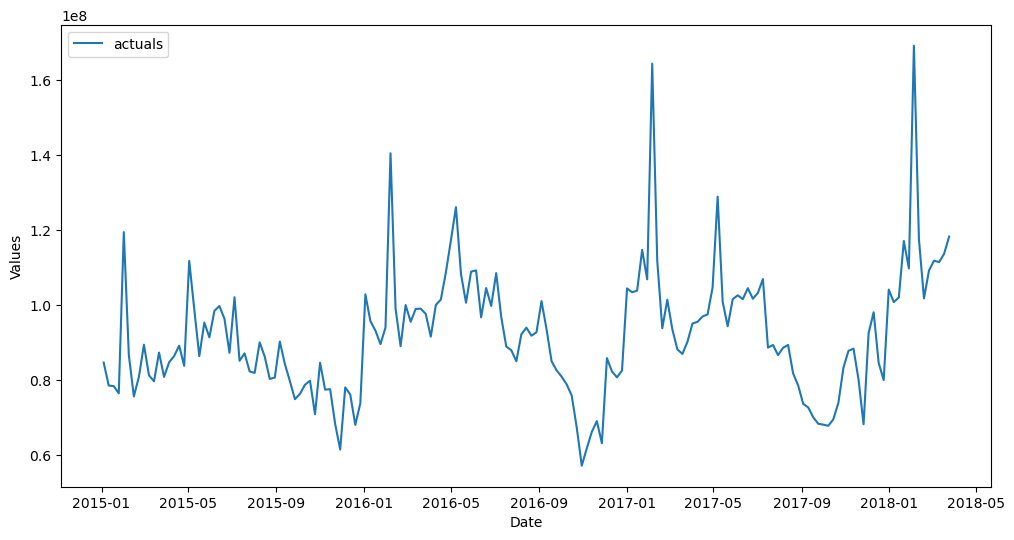

f.plot()

plt.show()

[7]:

plt.rc("figure",figsize=(10,6))

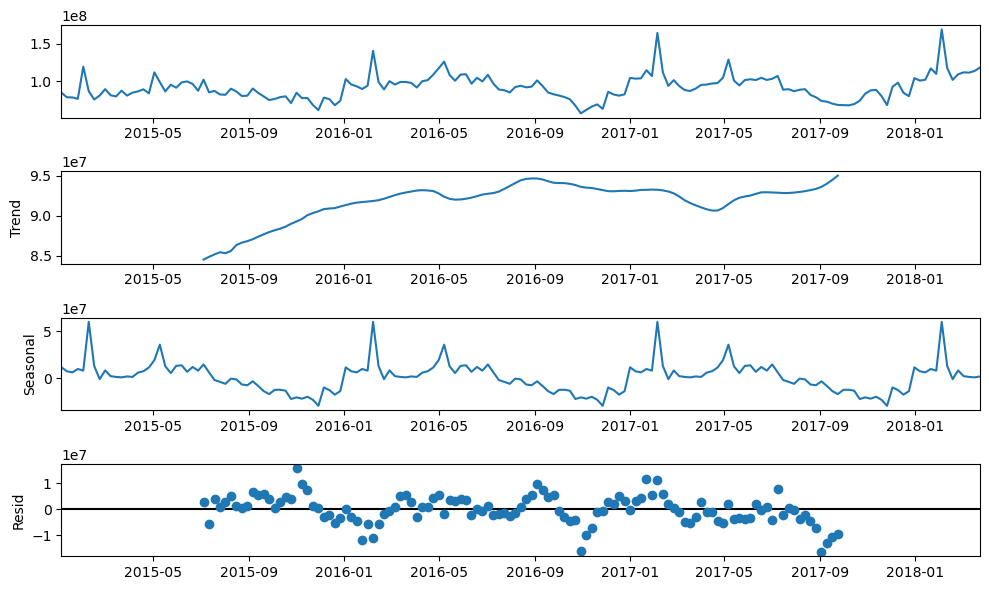

f.seasonal_decompose().plot()

plt.show()

[8]:

figs, axs = plt.subplots(2, 1,figsize=(9,9))

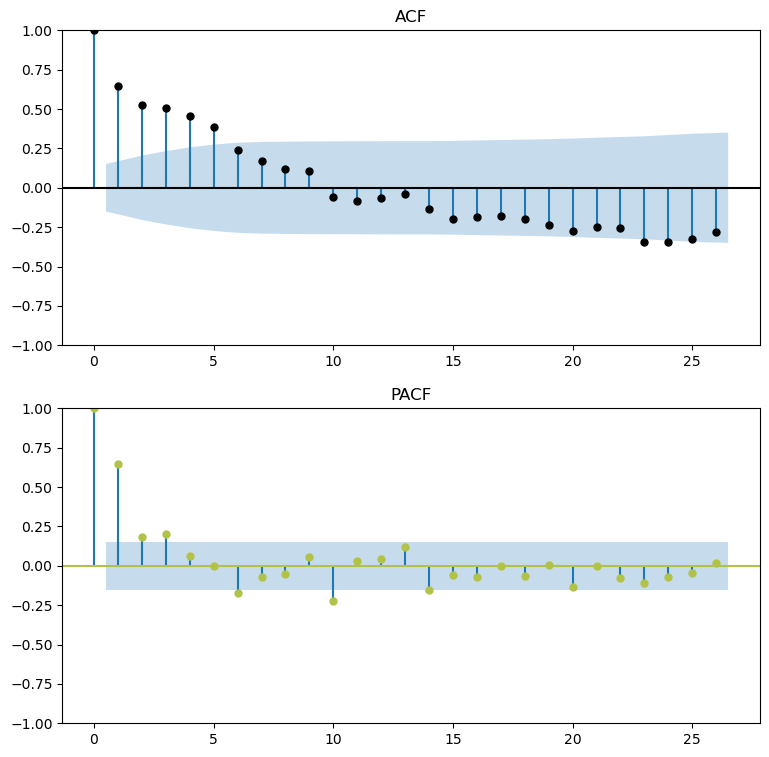

f.plot_acf(ax=axs[0],title='ACF',lags=26,color='black')

f.plot_pacf(ax=axs[1],title='PACF',lags=26,color='#B2C248',method='ywm')

plt.show()

Parameterize the Forecaster Object

Set Test Length

Starting in scalecast version 0.16.0, you can skip model testing by setting a test length of 0.

In this example, all models will be tested on the last 15% of the observed values in the dataset.

[9]:

f.set_test_length(.15)

Tell the Object to Evaluate Confidence Intervals

This only works if there is a test set specified and it is of a sufficient size.

See the documentation.

See the example.

[10]:

# default args below

f.eval_cis(

mode = True, # tell the object to evaluate intervals

cilevel = .95, # 95% confidence level

)

Specify Model Inputs

Trend

[11]:

f.add_time_trend()

Seasonality

[12]:

f.add_seasonal_regressors('week',raw=False,sincos=True)

Autoregressive Terms / Series Lags

[13]:

f.add_ar_terms(13)

[14]:

f

[14]:

Forecaster(

DateStartActuals=2015-01-04T00:00:00.000000000

DateEndActuals=2018-03-25T00:00:00.000000000

Freq=W-SUN

N_actuals=169

ForecastLength=13

Xvars=['t', 'weeksin', 'weekcos', 'AR1', 'AR2', 'AR3', 'AR4', 'AR5', 'AR6', 'AR7', 'AR8', 'AR9', 'AR10', 'AR11', 'AR12', 'AR13']

TestLength=25

ValidationMetric=rmse

ForecastsEvaluated=[]

CILevel=0.95

CurrentEstimator=mlr

GridsFile=Grids

)

Run Models

See the available models.

See the blog post.

The

dynamic_testingargument for all of these will be 13 – test-set results will then be in terms of rolling averages of 13-step forecasts, which is also our forecast length.The resulting forecasts from this process are not well-fit. Better forecasts are obtained once more optimization is performed in later sections.

Linear Scikit-Learn Models

[15]:

f.set_estimator('mlr')

f.manual_forecast(dynamic_testing=13)

[16]:

f.set_estimator('lasso')

f.manual_forecast(alpha=0.2,dynamic_testing=13)

[17]:

f.set_estimator('ridge')

f.manual_forecast(alpha=0.2,dynamic_testing=13)

[18]:

f.set_estimator('elasticnet')

f.manual_forecast(alpha=0.2,l1_ratio=0.5,dynamic_testing=13)

[19]:

f.set_estimator('sgd')

f.manual_forecast(alpha=0.2,l1_ratio=0.5,dynamic_testing=13)

[20]:

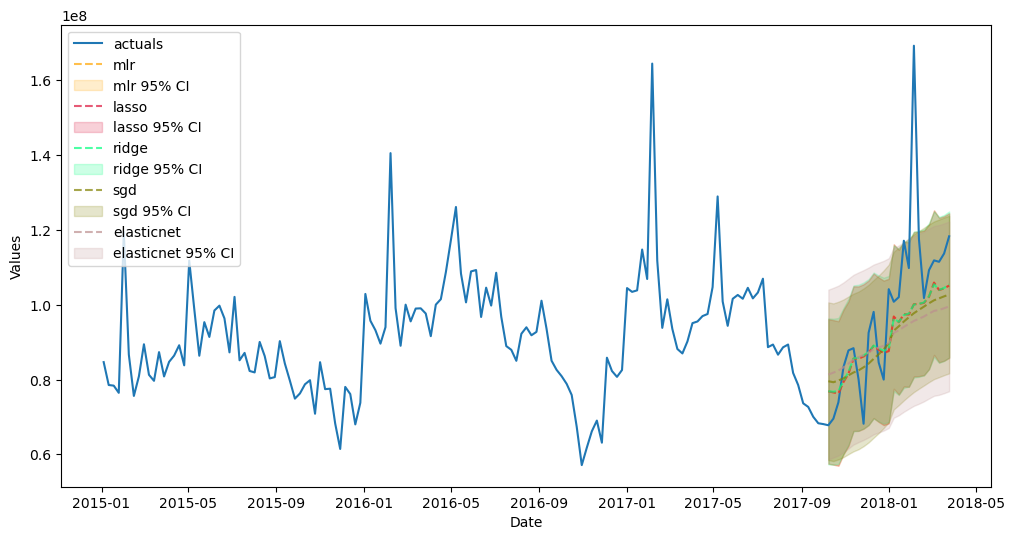

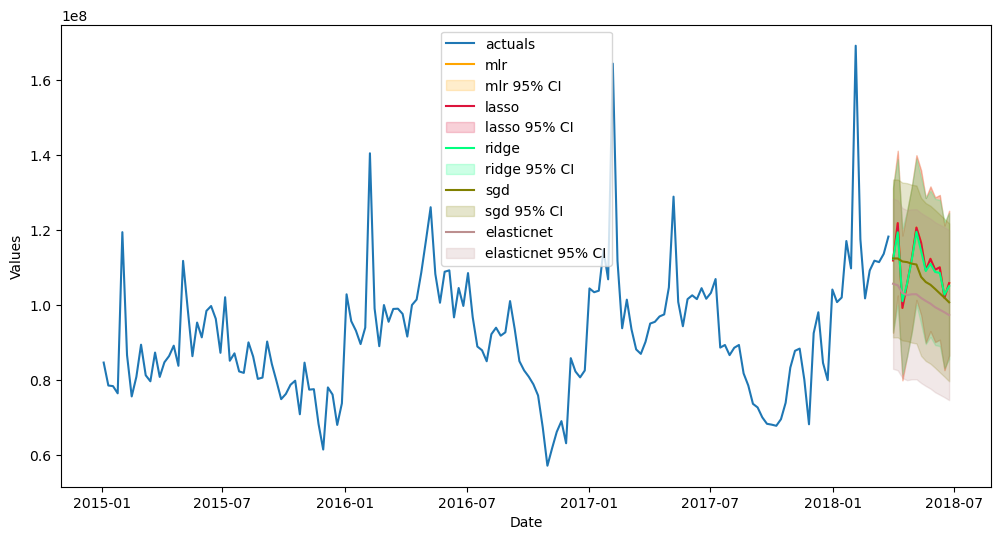

f.plot_test_set(ci=True,models=['mlr','lasso','ridge','elasticnet','sgd'],order_by='TestSetRMSE')

plt.show()

[21]:

f.plot(ci=True,models=['mlr','lasso','ridge','elasticnet','sgd'],order_by='TestSetRMSE')

plt.show()

Non-linear Scikit-Learn Models

[22]:

f.set_estimator('rf')

f.manual_forecast(max_depth=2,dynamic_testing=13)

[23]:

f.set_estimator('gbt')

f.manual_forecast(max_depth=2,dynamic_testing=13)

[24]:

f.set_estimator('xgboost')

f.manual_forecast(gamma=1,dynamic_testing=13)

[25]:

f.set_estimator('lightgbm')

f.manual_forecast(max_depth=2,dynamic_testing=13)

[26]:

f.set_estimator('catboost')

f.manual_forecast(depth=4,verbose=False,dynamic_testing=13)

Finished loading model, total used 100 iterations

[27]:

f.set_estimator('knn')

f.manual_forecast(n_neighbors=5,dynamic_testing=13)

Finished loading model, total used 100 iterations

[28]:

f.set_estimator('mlp')

f.manual_forecast(hidden_layer_sizes=(50,50),solver='lbfgs',dynamic_testing=13)

Finished loading model, total used 100 iterations

[29]:

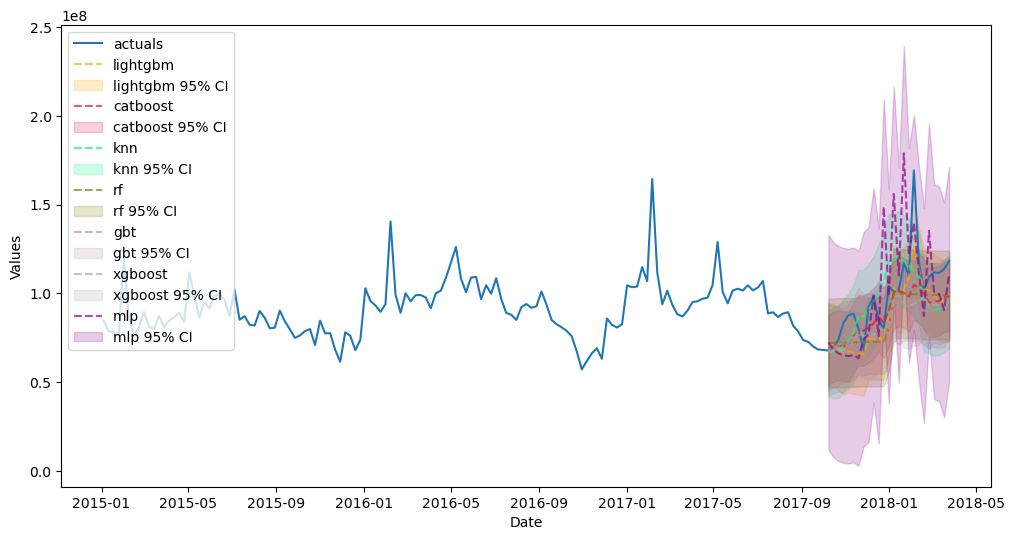

f.plot_test_set(

ci=True,

models=['rf','gbt','xgboost','lightgbm','catboost','knn','mlp'],

order_by='TestSetRMSE'

)

plt.show()

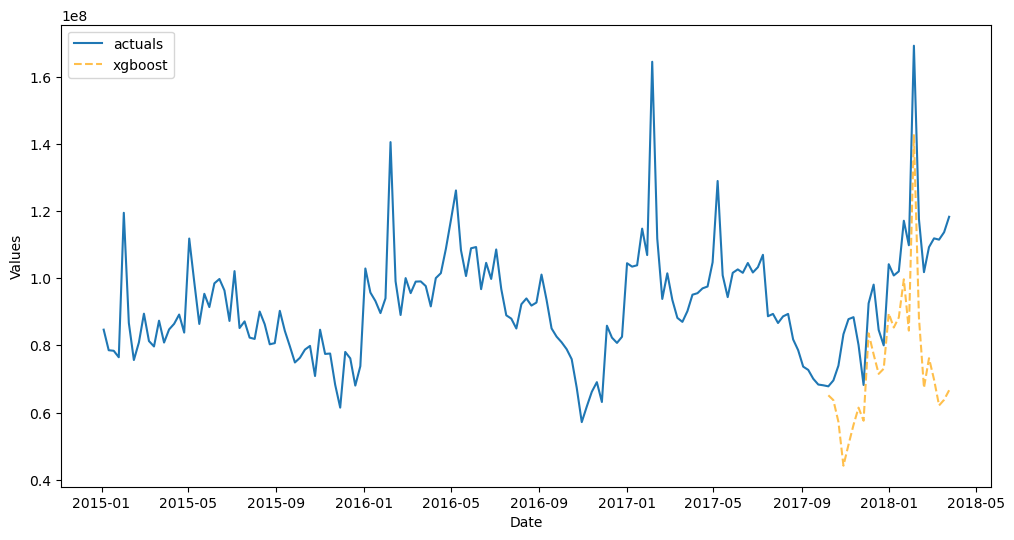

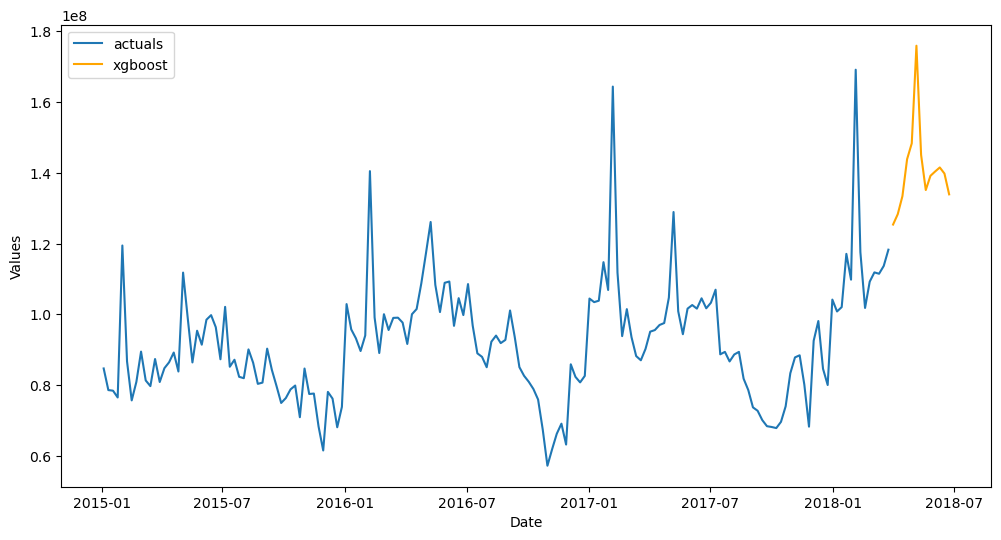

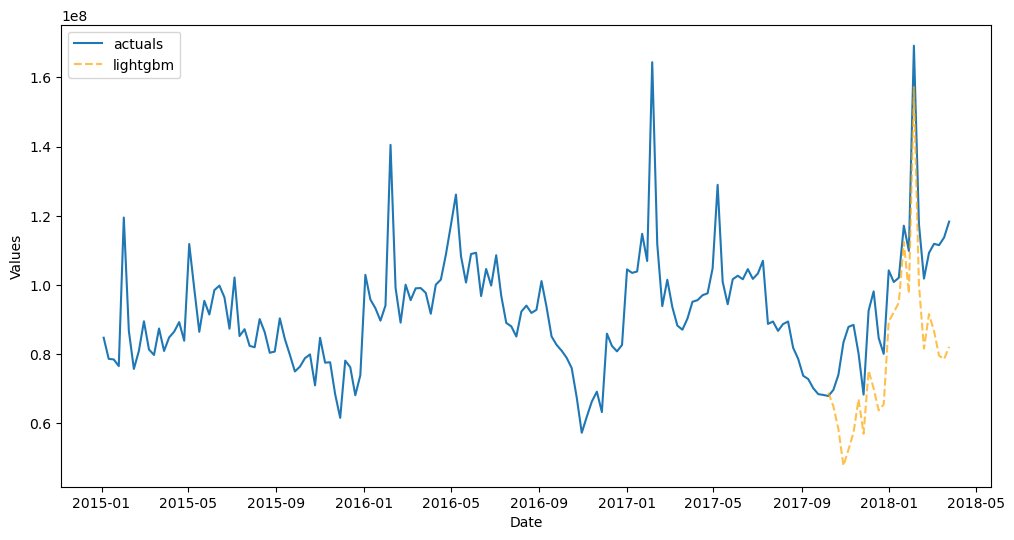

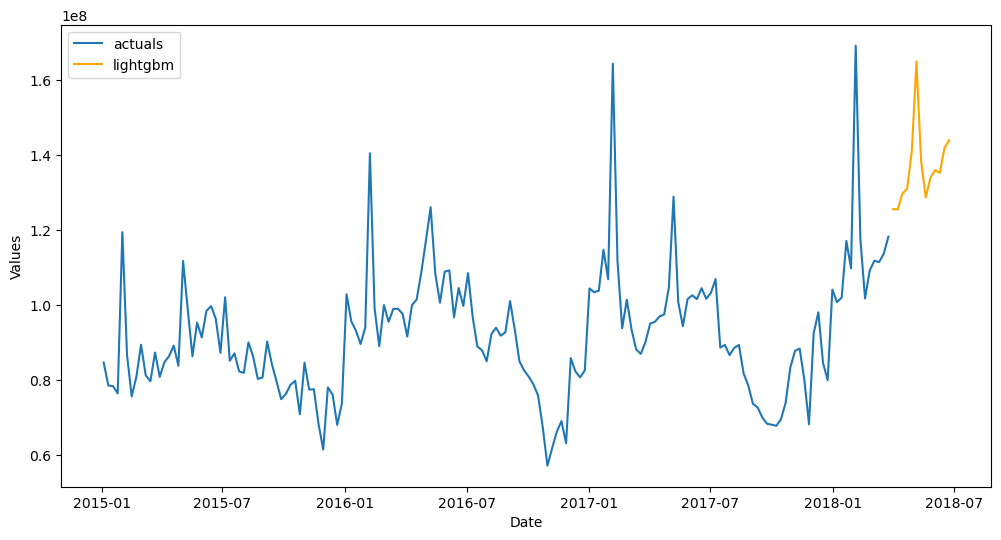

[30]:

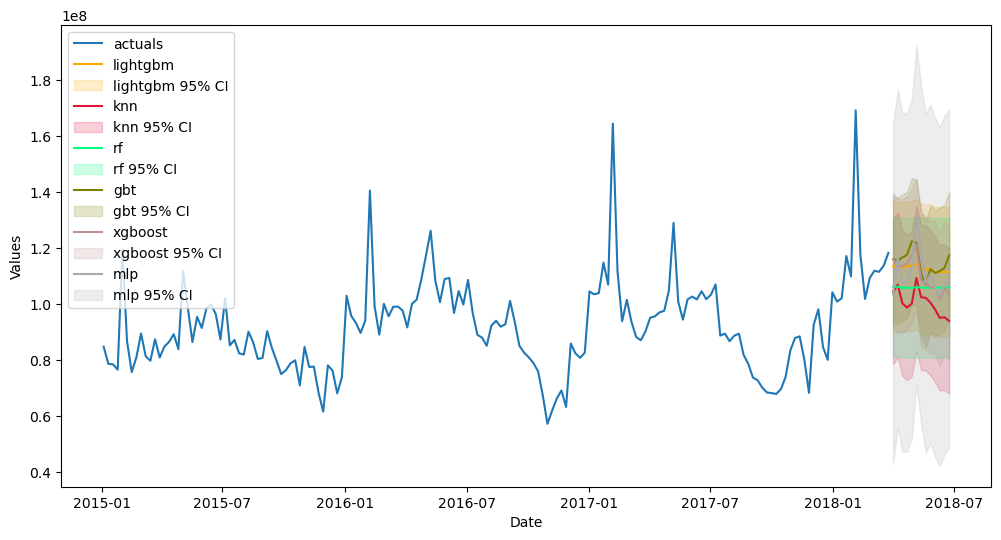

f.plot(ci=True,models=['rf','gbt','xgboost','lightgbm','knn','mlp'],order_by='TestSetRMSE')

plt.show()

Stacking Models

Sklearn Stacking Model

[31]:

from sklearn.ensemble import StackingRegressor

from sklearn.linear_model import SGDRegressor

from sklearn.linear_model import ElasticNet

from sklearn.ensemble import GradientBoostingRegressor

from sklearn.neighbors import KNeighborsRegressor

from xgboost import XGBRegressor

from lightgbm import LGBMRegressor

[32]:

f.add_sklearn_estimator(StackingRegressor,'stacking')

[33]:

estimators = [

('elasticnet',ElasticNet(alpha=0.2)),

('xgboost',XGBRegressor(gamma=1)),

('gbt',GradientBoostingRegressor(max_depth=2)),

]

final_estimator = LGBMRegressor()

f.set_estimator('stacking')

f.manual_forecast(

estimators=estimators,

final_estimator=final_estimator,

dynamic_testing=13

)

Finished loading model, total used 100 iterations

Scalecast Stacking Model

[34]:

f.add_signals(['elasticnet','lightgbm','xgboost','knn'],train_only=True)

f.set_estimator('catboost')

f.manual_forecast(call_me = 'catboost_stack',verbose=False)

Finished loading model, total used 100 iterations

Finished loading model, total used 100 iterations

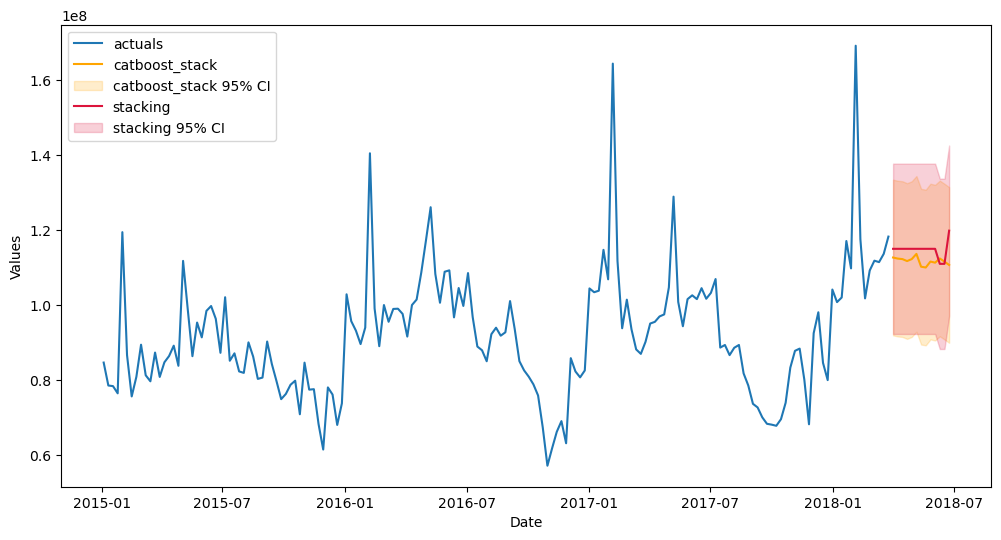

[35]:

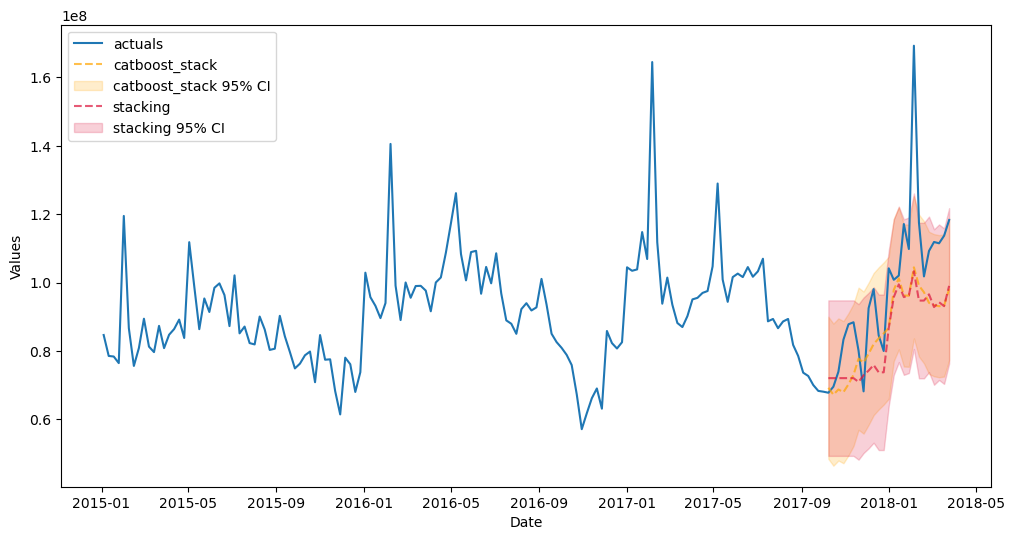

f.plot_test_set(models=['stacking','catboost_stack'],ci=True,order_by='TestSetRMSE')

plt.show()

[36]:

f.plot(models=['stacking','catboost_stack'],ci=True,order_by='TestSetRMSE')

plt.show()

ARIMA

[37]:

from scalecast.auxmodels import auto_arima

[38]:

auto_arima(f,m=52)

Finished loading model, total used 100 iterations

Finished loading model, total used 100 iterations

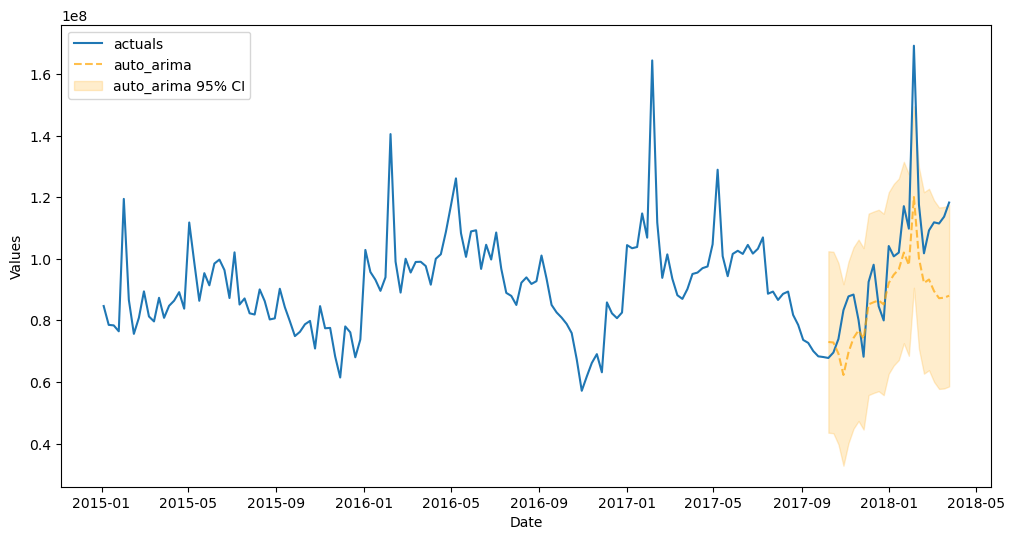

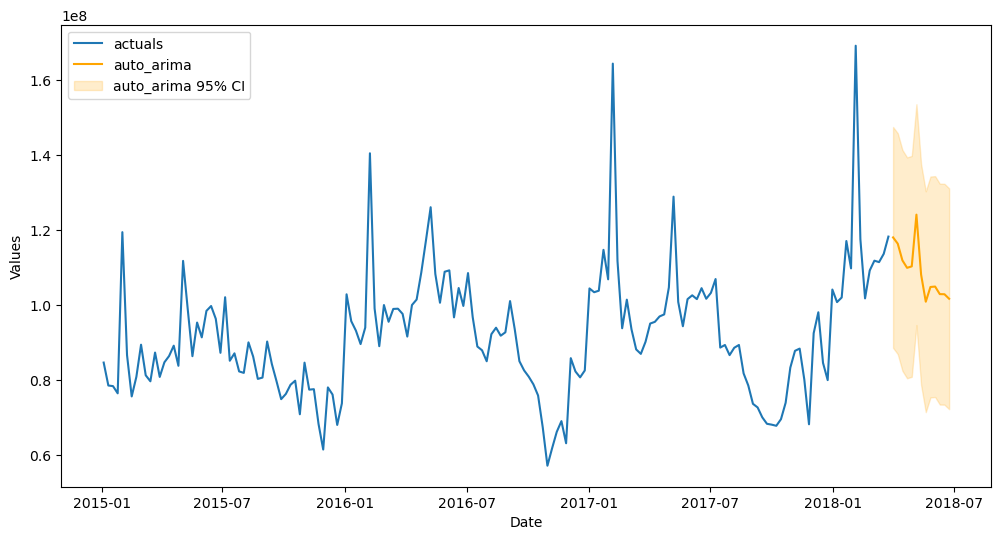

[39]:

f.plot_test_set(models='auto_arima',ci=True)

plt.show()

[40]:

f.plot(models='auto_arima',ci=True)

plt.show()

Prophet

[41]:

f.set_estimator('prophet')

f.manual_forecast()

Finished loading model, total used 100 iterations

Finished loading model, total used 100 iterations

22:14:17 - cmdstanpy - INFO - Chain [1] start processing

22:14:17 - cmdstanpy - INFO - Chain [1] done processing

22:14:17 - cmdstanpy - INFO - Chain [1] start processing

22:14:17 - cmdstanpy - INFO - Chain [1] done processing

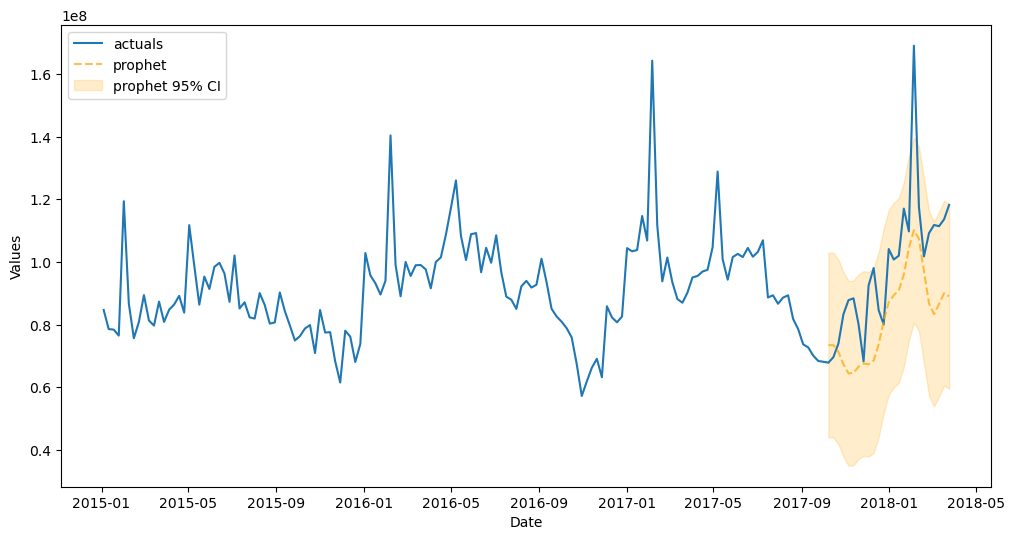

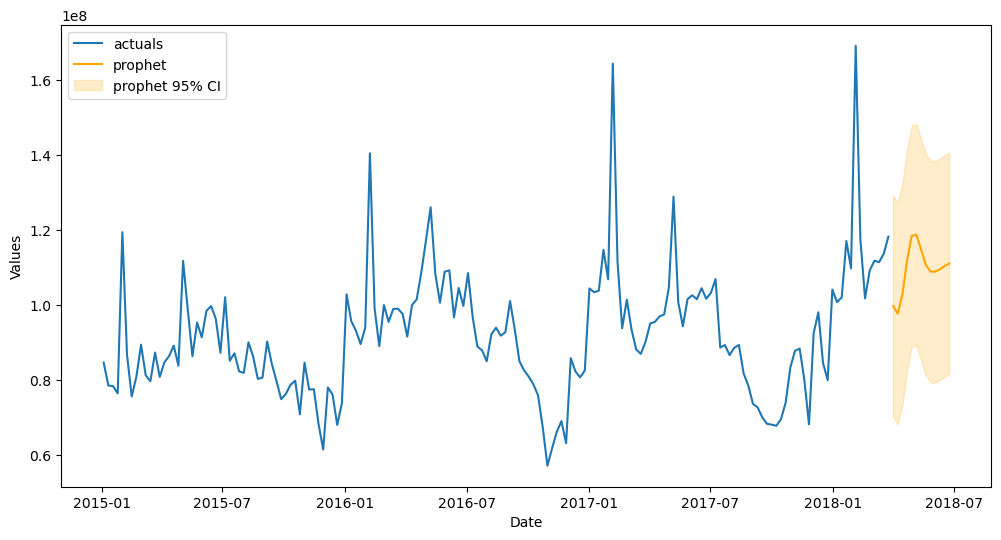

[42]:

f.plot_test_set(models='prophet',ci=True)

plt.show()

[43]:

f.plot(models='prophet',ci=True)

plt.show()

Other univariate models available: TBATS, Holt-Winters Exponential Smoothing, LSTM, RNN, Silverkite, Theta.

Working on: N-Beats, N-Hits, Genetic Algorithm.

Multivariate Forecasting

Load the MVForecaster Object

This object extends the univariate approach to several series, with many of the same plotting and reporting features available.

[44]:

from scalecast.MVForecaster import MVForecaster

[45]:

price = data.groupby('Date')['AveragePrice'].mean()

fvol = Forecaster(y=volume,current_dates=volume.index,future_dates=13)

fprice = Forecaster(y=price,current_dates=price.index,future_dates=13)

fvol.add_time_trend()

fvol.add_seasonal_regressors('week',raw=False,sincos=True)

mvf = MVForecaster(

fvol,

fprice,

merge_Xvars='union',

names=['volume','price'],

)

mvf

[45]:

MVForecaster(

DateStartActuals=2015-01-04T00:00:00.000000000

DateEndActuals=2018-03-25T00:00:00.000000000

Freq=W-SUN

N_actuals=169

N_series=2

SeriesNames=['volume', 'price']

ForecastLength=13

Xvars=['t', 'weeksin', 'weekcos']

TestLength=0

ValidationLength=1

ValidationMetric=rmse

ForecastsEvaluated=[]

CILevel=None

CurrentEstimator=mlr

OptimizeOn=mean

GridsFile=MVGrids

)

Exploratory Data Analysis

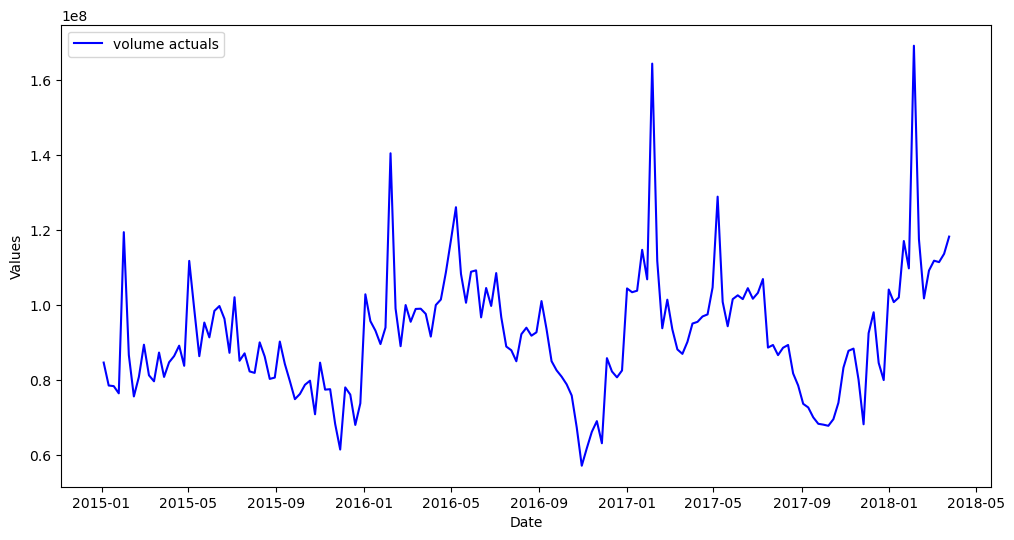

[46]:

mvf.plot(series='volume')

plt.show()

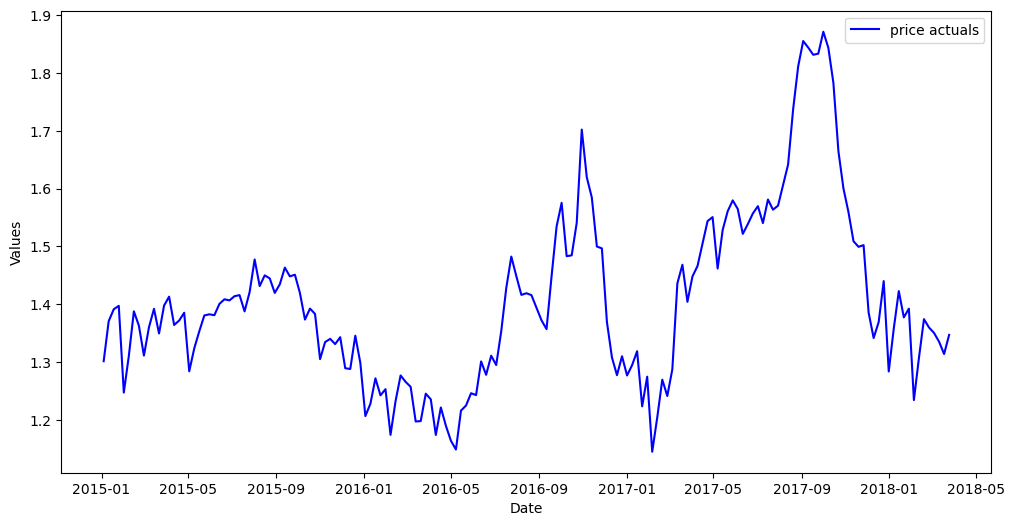

[47]:

mvf.plot(series='price')

plt.show()

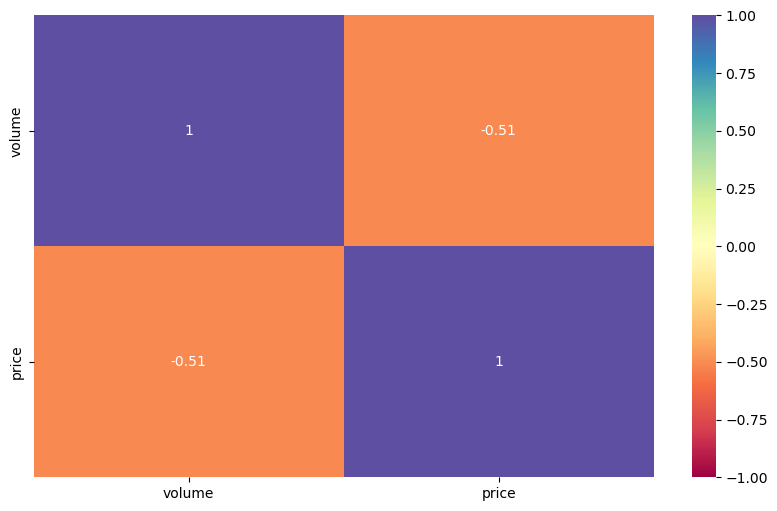

[48]:

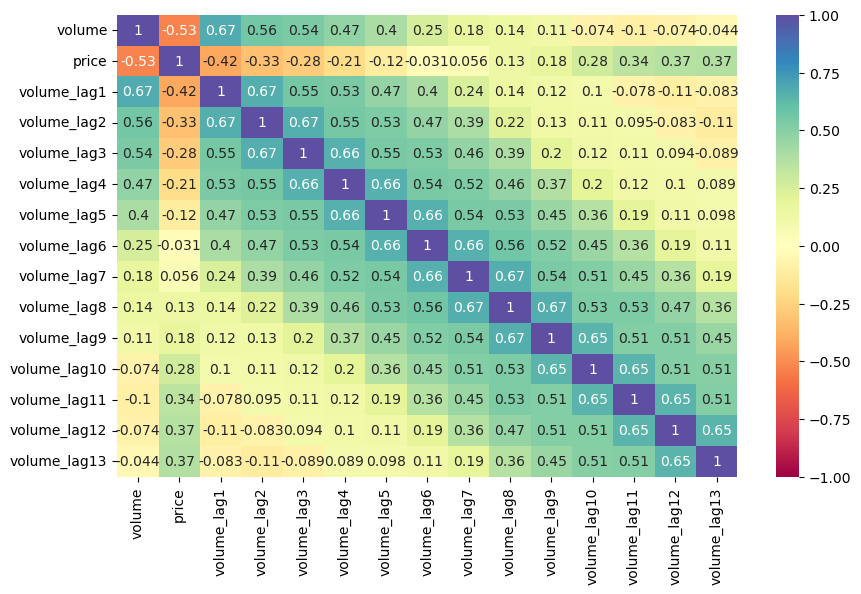

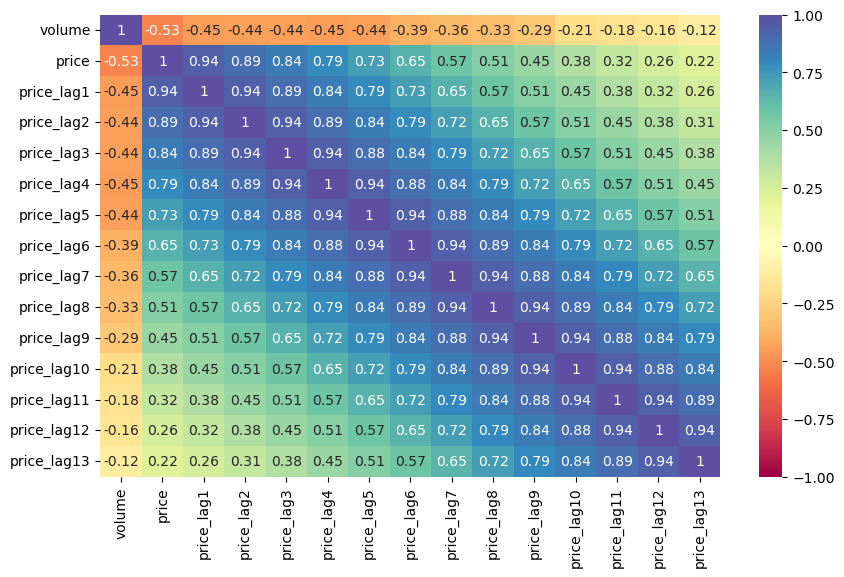

mvf.corr(disp='heatmap',cmap='Spectral',annot=True,vmin=-1,vmax=1)

plt.show()

[49]:

mvf.corr_lags(y='price',x='volume',disp='heatmap',cmap='Spectral',annot=True,vmin=-1,vmax=1,lags=13)

plt.show()

[50]:

mvf.corr_lags(y='volume',x='price',disp='heatmap',cmap='Spectral',annot=True,vmin=-1,vmax=1,lags=13)

plt.show()

Parameterize the MVForecaster Object

Starting in scalecast version 0.16.0, you can skip model testing by setting a test length of 0.

In this example, all models will be tested on the last 15% of the observed values in the dataset.

We will also have model optimization select hyperparemeters based on what predicts the volume series, rather than the price series, or an average of the two (which is the default), best.

Custom optimization functions are available.

[51]:

mvf.set_test_length(.15)

mvf.set_optimize_on('volume') # we care more about predicting volume and price is just used to make those predictions more accurate

# by default, the optimizer uses an average scoring of all series in the MVForecaster object

mvf.eval_cis() # tell object to evaluate cis

mvf

[51]:

MVForecaster(

DateStartActuals=2015-01-04T00:00:00.000000000

DateEndActuals=2018-03-25T00:00:00.000000000

Freq=W-SUN

N_actuals=169

N_series=2

SeriesNames=['volume', 'price']

ForecastLength=13

Xvars=['t', 'weeksin', 'weekcos']

TestLength=25

ValidationLength=1

ValidationMetric=rmse

ForecastsEvaluated=[]

CILevel=0.95

CurrentEstimator=mlr

OptimizeOn=volume

GridsFile=MVGrids

)

Run Models

Uses scikit-learn models and APIs only.

See the adapted VECM model for this object.

ElasticNet

[52]:

mvf.set_estimator('elasticnet')

mvf.manual_forecast(alpha=0.2,dynamic_testing=13,lags=13)

XGBoost

[53]:

mvf.set_estimator('xgboost')

mvf.manual_forecast(gamma=1,dynamic_testing=13,lags=13)

MLP Stack

[54]:

from scalecast.auxmodels import mlp_stack

[55]:

mvf.export('model_summaries')

[55]:

| Series | ModelNickname | Estimator | Xvars | HyperParams | Lags | Observations | DynamicallyTested | TestSetLength | ValidationMetric | ValidationMetricValue | InSampleRMSE | InSampleMAPE | InSampleMAE | InSampleR2 | TestSetRMSE | TestSetMAPE | TestSetMAE | TestSetR2 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | volume | elasticnet | elasticnet | [t, weeksin, weekcos] | {'alpha': 0.2} | 13 | 169 | 13 | 25 | NaN | NaN | 1.197603e+07 | 0.088917 | 8.206334e+06 | 0.486109 | 1.869490e+07 | 0.118172 | 1.282436e+07 | 0.248765 |

| 1 | volume | xgboost | xgboost | [t, weeksin, weekcos] | {'gamma': 1} | 13 | 169 | 13 | 25 | NaN | NaN | 3.416022e+02 | 0.000003 | 2.591667e+02 | 1.000000 | 2.260606e+07 | 0.173554 | 1.644149e+07 | -0.098447 |

| 2 | price | elasticnet | elasticnet | [t, weeksin, weekcos] | {'alpha': 0.2} | 13 | 169 | 13 | 25 | NaN | NaN | 1.560728e-01 | 0.084080 | 1.199107e-01 | 0.000000 | 1.522410e-01 | 0.071282 | 1.088633e-01 | -0.048569 |

| 3 | price | xgboost | xgboost | [t, weeksin, weekcos] | {'gamma': 1} | 13 | 169 | 13 | 25 | NaN | NaN | 1.141005e-01 | 0.058215 | 8.255353e-02 | 0.465533 | 1.291758e-01 | 0.057186 | 8.791148e-02 | 0.245089 |

[56]:

mlp_stack(mvf,model_nicknames=['elasticnet','xgboost'],lags=13)

[57]:

mvf.set_best_model(determine_best_by='TestSetRMSE')

[58]:

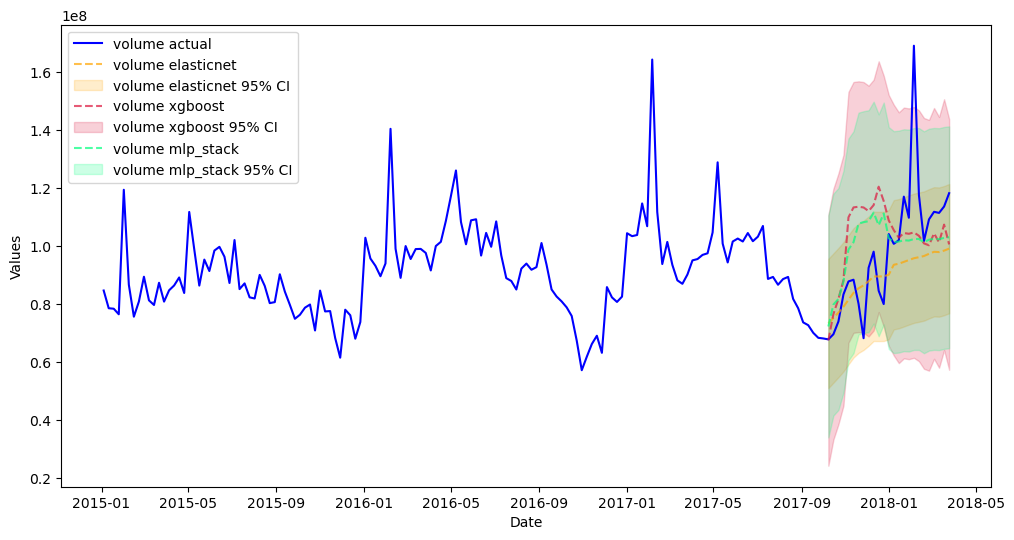

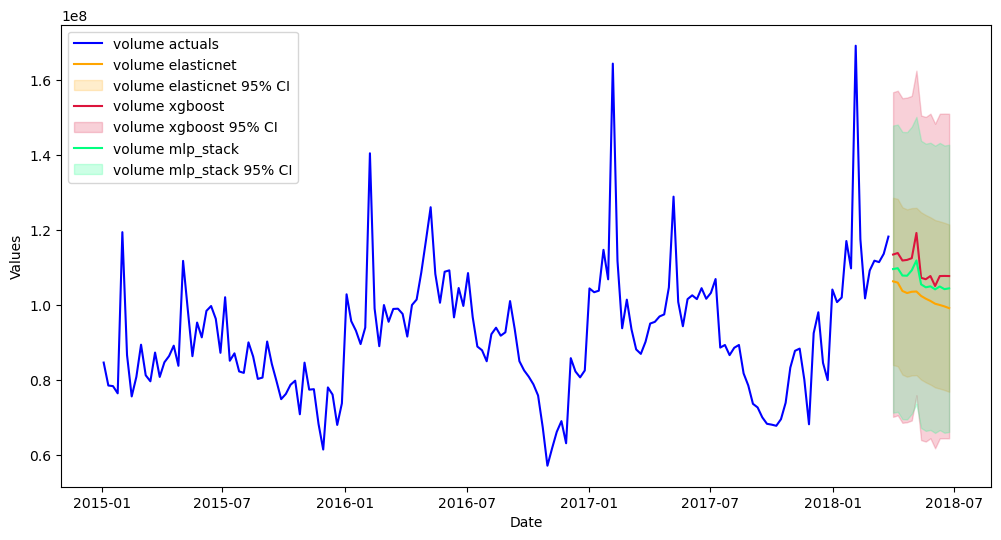

mvf.plot_test_set(ci=True,series='volume',put_best_on_top=True)

plt.show()

[59]:

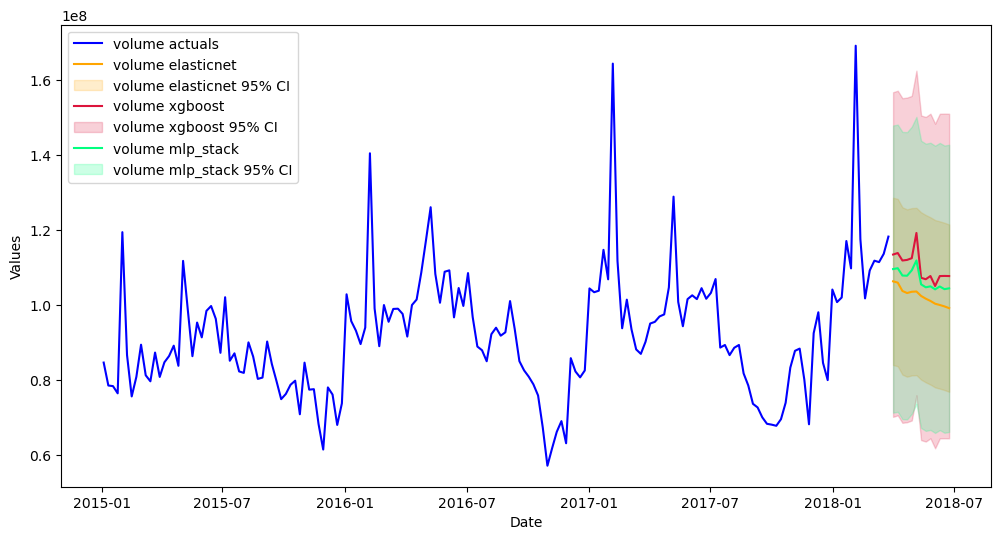

mvf.plot(ci=True,series='volume',put_best_on_top=True)

plt.show()

Probabalistic forecasting for creating confidence intervals is currently being worked on in the MVForecaster object, but until that is done, the backtested interval also works well:

[60]:

mvf.plot(ci=True,series='volume',put_best_on_top=True)

plt.show()

Break Back into Forecaster Objects

You can then add univariate models to these objects to compare with the models run multivariate.

[61]:

from scalecast.util import break_mv_forecaster

[62]:

fvol, fprice = break_mv_forecaster(mvf)

[63]:

fvol

[63]:

Forecaster(

DateStartActuals=2015-01-04T00:00:00.000000000

DateEndActuals=2018-03-25T00:00:00.000000000

Freq=W-SUN

N_actuals=169

ForecastLength=13

Xvars=[]

TestLength=25

ValidationMetric=rmse

ForecastsEvaluated=['elasticnet', 'xgboost', 'mlp_stack']

CILevel=0.95

CurrentEstimator=mlr

GridsFile=Grids

)

[64]:

fprice

[64]:

Forecaster(

DateStartActuals=2015-01-04T00:00:00.000000000

DateEndActuals=2018-03-25T00:00:00.000000000

Freq=W-SUN

N_actuals=169

ForecastLength=13

Xvars=[]

TestLength=25

ValidationMetric=rmse

ForecastsEvaluated=['elasticnet', 'xgboost', 'mlp_stack']

CILevel=0.95

CurrentEstimator=mlr

GridsFile=Grids

)

Transformations

One of the most effective way to boost forecasting power is with transformations.

Transformations include:

Scaling

All transformations have a corresponding revert function.

See the blog post.

[65]:

from scalecast.SeriesTransformer import SeriesTransformer

[66]:

f_trans = Forecaster(y=volume,current_dates=volume.index,future_dates=13)

[67]:

f_trans.set_test_length(.15)

f_trans.set_validation_length(13)

[68]:

transformer = SeriesTransformer(f_trans)

[69]:

# these will all be reverted later after forecasts have been called

f_trans = transformer.DiffTransform(1)

f_trans = transformer.DiffTransform(52)

f_trans = transformer.DetrendTransform()

[70]:

f_trans.plot()

plt.show()

[71]:

f_trans.add_time_trend()

f_trans.add_seasonal_regressors('week',sincos=True,raw=False)

f_trans.add_ar_terms(13)

[72]:

f_trans.set_estimator('xgboost')

f_trans.manual_forecast(gamma=1,dynamic_testing=13)

[73]:

f_trans.plot_test_set()

plt.show()

[74]:

f_trans.plot()

plt.show()

[75]:

# call revert functions in the opposite order as how they were called when transforming

f_trans = transformer.DetrendRevert()

f_trans = transformer.DiffRevert(52)

f_trans = transformer.DiffRevert(1)

[76]:

f_trans.plot_test_set()

plt.show()

[77]:

f_trans.plot()

plt.show()

Pipelines

These are objects similar to scikit-learn pipelines that offer readable and streamlined code for transforming, forecasting, and reverting.

See the Pipeline object documentation.

[78]:

from scalecast.Pipeline import Transformer, Reverter, Pipeline, MVPipeline

[79]:

f_pipe = Forecaster(y=volume,current_dates=volume.index,future_dates=13)

f_pipe.set_test_length(.15)

[80]:

def forecaster(f):

f.add_time_trend()

f.add_seasonal_regressors('week',raw=False,sincos=True)

f.add_ar_terms(13)

f.set_estimator('lightgbm')

f.manual_forecast(max_depth=2)

[81]:

transformer = Transformer(

transformers = [

('DiffTransform',1),

('DiffTransform',52),

('DetrendTransform',)

]

)

reverter = Reverter(

reverters = [

('DetrendRevert',),

('DiffRevert',52),

('DiffRevert',1)

],

base_transformer = transformer,

)

[82]:

reverter

[82]:

Reverter(

reverters = [

('DetrendRevert',),

('DiffRevert', 52),

('DiffRevert', 1)

],

base_transformer = Transformer(

transformers = [

('DiffTransform', 1),

('DiffTransform', 52),

('DetrendTransform',)

]

)

)

[83]:

pipeline = Pipeline(

steps = [

('Transform',transformer),

('Forecast',forecaster),

('Revert',reverter),

]

)

f_pipe = pipeline.fit_predict(f_pipe)

[84]:

f_pipe.plot_test_set()

plt.show()

[85]:

f_pipe.plot()

plt.show()

Fully Automated Pipelines

We can automate the construction of pipelines, the selection of input variables, and tuning of models with cross validation on a grid search for each model using files in the working directory called

Grids.pyfor univariate forecasting andMVGrids.pyfor multivariate. Default grids can be downloaded from scalecast.

Automated Univariate Pipelines

[86]:

from scalecast import GridGenerator

from scalecast.util import find_optimal_transformation

[87]:

GridGenerator.get_example_grids(overwrite=True)

[88]:

f_pipe_aut = Forecaster(y=volume,current_dates=volume.index,future_dates=13)

f_pipe_aut.set_test_length(.15)

[89]:

def forecaster_aut(f,models):

f.auto_Xvar_select(

estimator='elasticnet',

monitor='TestSetMAE',

alpha=0.2,

irr_cycles = [26],

)

f.tune_test_forecast(

models,

cross_validate=True,

k=3,

# dynamic tuning = 13 means we will hopefully find a model that is optimized to predict 13 steps

dynamic_tuning=13,

dynamic_testing=13,

)

f.set_estimator('combo')

f.manual_forecast()

util.find_optimal_transformation

The optimal set of transformations are returned based on best estimated out-of-sample performance on the test set. Therefore, running this function introduces leakage into the test set, but it can still be a good addition to an automated pipeline, depending on the application. Which and the order of transfomations to search through are configurable. How performance is measured, the parameters specific to a given transformation, and several other paramters are also configurable. See the documentation.

[90]:

transformer_aut, reverter_aut = find_optimal_transformation(

f_pipe_aut,

lags = 13,

m = 52,

monitor = 'mae',

estimator = 'elasticnet',

alpha = 0.2,

test_length = 13,

num_test_sets = 3,

space_between_sets = 4,

verbose = True,

) # returns a Transformer and Reverter object that can be plugged into a larger pipeline

All transformation tries will use 13 lags.

Last transformer tried:

[]

Score (mae): 17933061.20374991

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'loess': True})]

Score (mae): 23964157.165726673

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1})]

Score (mae): 17174376.36667074

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 2})]

Score (mae): 24467364.037868027

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'})]

Score (mae): 11573053.425807403

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 1)]

Score (mae): 9478522.651025781

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 1), ('DiffTransform', 52)]

Score (mae): 11116081.856823219

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 1), ('ScaleTransform',)]

Score (mae): 9583504.942193026

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 1), ('MinMaxTransform',)]

Score (mae): 9583504.942193048

--------------------------------------------------

Final Selection:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 1)]

[91]:

pipeline_aut = Pipeline(

steps = [

('Transform',transformer_aut),

('Forecast',forecaster_aut),

('Revert',reverter_aut),

]

)

f_pipe_aut = pipeline_aut.fit_predict(

f_pipe_aut,

models=[

'mlr',

'elasticnet',

'xgboost',

'lightgbm',

'knn',

],

)

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

[92]:

f_pipe_aut

[92]:

Forecaster(

DateStartActuals=2015-01-04T00:00:00.000000000

DateEndActuals=2018-03-25T00:00:00.000000000

Freq=W-SUN

N_actuals=169

ForecastLength=13

Xvars=['AR1', 'AR2', 'AR3', 'AR4', 'AR5']

TestLength=25

ValidationMetric=rmse

ForecastsEvaluated=['mlr', 'elasticnet', 'xgboost', 'lightgbm', 'knn', 'combo']

CILevel=None

CurrentEstimator=combo

GridsFile=Grids

)

[93]:

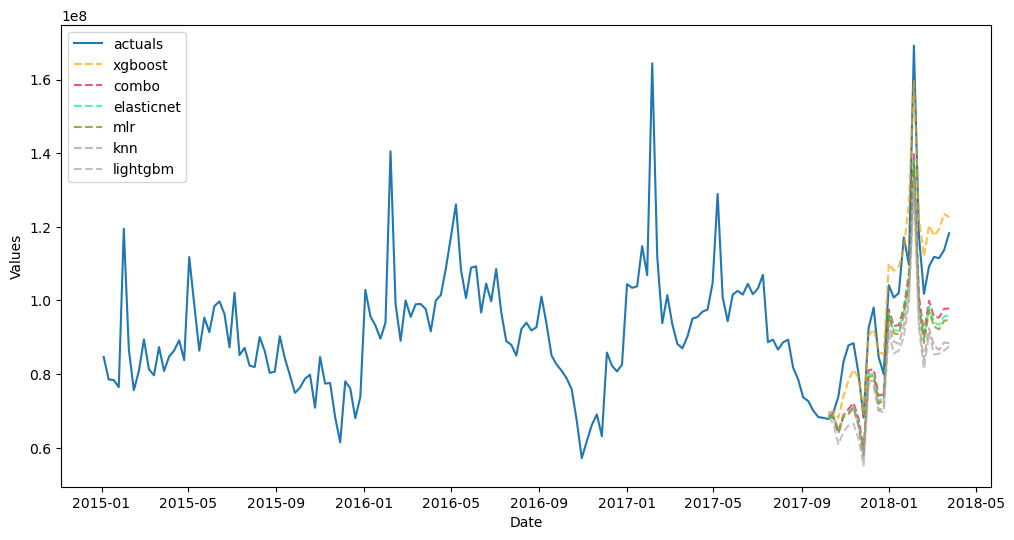

f_pipe_aut.plot_test_set(order_by='TestSetRMSE')

plt.show()

[94]:

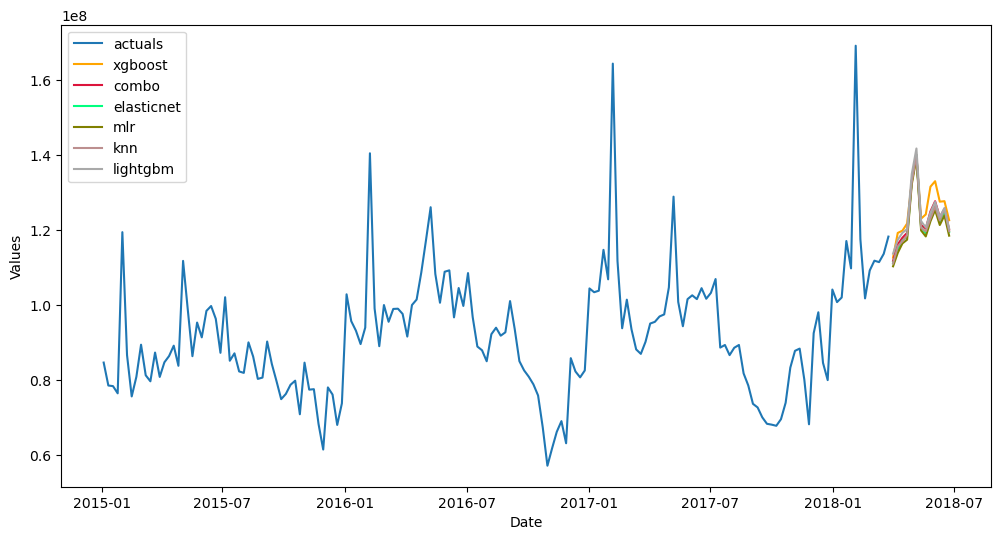

f_pipe_aut.plot(order_by='TestSetRMSE')

plt.show()

Backtest Univariate Pipeline

You may be interested to know beyond a single test-set metric, how well your pipeline performs out-of-sample. Backtesting can help answer that by iterating through the entire pipeline several times and testing the procedure each time. It can also help make expanding confidence intervals. See the documentation.

[95]:

from scalecast.util import backtest_metrics

[96]:

uv_backtest_results = pipeline_aut.backtest(

f_pipe_aut,

n_iter = 3,

jump_back = 13,

cis = False,

models=[

'mlr',

'elasticnet',

'xgboost',

'lightgbm',

'knn',

],

)

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

After obtaining the results from the backtest, we can see the average performance over each iteration using the util.backtest_metrics function. See the documentation.

[97]:

pd.options.display.float_format = '{:,.4f}'.format

backtest_metrics(

uv_backtest_results,

mets=['smape','rmse','bias'],

)

[97]:

| Iter0 | Iter1 | Iter2 | Average | ||

|---|---|---|---|---|---|

| Model | Metric | ||||

| mlr | smape | 0.1130 | 0.2317 | 0.1142 | 0.1529 |

| rmse | 15,488,744.6687 | 19,538,227.8483 | 11,910,709.6300 | 15,645,894.0490 | |

| bias | -165,115,026.5519 | -207,268,257.9313 | 103,757,419.4097 | -89,541,955.0245 | |

| elasticnet | smape | 0.1237 | 0.1962 | 0.1428 | 0.1542 |

| rmse | 16,732,592.7781 | 16,625,313.2954 | 14,338,412.2989 | 15,898,772.7908 | |

| bias | -177,765,519.3932 | -169,974,287.0231 | 145,808,728.0805 | -67,310,359.4453 | |

| xgboost | smape | 0.0978 | 0.2221 | 0.1710 | 0.1636 |

| rmse | 13,607,549.8360 | 18,573,088.5135 | 18,136,645.4700 | 16,772,427.9399 | |

| bias | -139,025,946.3310 | -187,065,120.1406 | 180,813,791.1197 | -48,425,758.4506 | |

| lightgbm | smape | 0.1248 | 0.2178 | 0.1483 | 0.1636 |

| rmse | 16,803,405.5145 | 18,415,746.1087 | 15,074,267.8093 | 16,764,473.1442 | |

| bias | -176,880,323.1388 | -195,683,280.2443 | 149,272,223.4129 | -74,430,459.9901 | |

| knn | smape | 0.2044 | 0.1896 | 0.1439 | 0.1793 |

| rmse | 23,802,323.7447 | 16,441,684.0561 | 14,418,665.8740 | 18,220,891.2249 | |

| bias | -278,780,122.9043 | -174,089,027.5994 | 145,204,593.3703 | -102,554,852.3778 | |

| combo | smape | 0.1304 | 0.2109 | 0.1438 | 0.1617 |

| rmse | 17,124,663.5858 | 17,869,415.4842 | 14,723,986.4866 | 16,572,688.5189 | |

| bias | -187,513,387.6638 | -186,815,994.5877 | 144,971,351.0786 | -76,452,677.0576 |

Automated Multivariate Pipelines

See the MVPipeline object documentation.

[98]:

GridGenerator.get_mv_grids(overwrite=True)

[99]:

fvol_aut = Forecaster(

y=volume,

current_dates=volume.index,

future_dates=13,

test_length = .15,

)

fprice_aut = Forecaster(

y=price,

current_dates=price.index,

future_dates=13,

test_length = .15,

)

[100]:

def add_vars(f,**kwargs):

f.add_seasonal_regressors(

'month',

'quarter',

'week',

raw=False,

sincos=True

)

def mvforecaster(mvf,models):

mvf.set_optimize_on('volume')

mvf.tune_test_forecast(

models,

cross_validate=True,

k=2,

rolling=True,

dynamic_tuning=13,

dynamic_testing=13,

limit_grid_size = .2,

error = 'warn',

)

[101]:

transformer_vol, reverter_vol = find_optimal_transformation(

fvol_aut,

lags = 13,

m = 52,

monitor = 'mae',

estimator = 'elasticnet',

alpha = 0.2,

test_length = 13,

num_test_sets = 3,

space_between_sets = 4,

verbose = True,

)

All transformation tries will use 13 lags.

Last transformer tried:

[]

Score (mae): 17933061.20374991

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'loess': True})]

Score (mae): 23964157.165726673

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1})]

Score (mae): 17174376.36667074

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 2})]

Score (mae): 24467364.037868027

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'})]

Score (mae): 11573053.425807403

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 1)]

Score (mae): 9478522.651025781

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 1), ('DiffTransform', 52)]

Score (mae): 11116081.856823219

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 1), ('ScaleTransform',)]

Score (mae): 9583504.942193026

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 1), ('MinMaxTransform',)]

Score (mae): 9583504.942193048

--------------------------------------------------

Final Selection:

[('DetrendTransform', {'poly_order': 1}), ('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 1)]

[102]:

transformer_price, reverter_price = find_optimal_transformation(

fprice_aut,

lags = 13,

m = 52,

monitor = 'mae',

estimator = 'elasticnet',

alpha = 0.2,

test_length = 13,

num_test_sets = 3,

space_between_sets = 4,

verbose = True,

)

All transformation tries will use 13 lags.

Last transformer tried:

[]

Score (mae): 0.06804292152560591

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'loess': True})]

Score (mae): 0.35311292233215247

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1})]

Score (mae): 0.18654572266988656

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 2})]

Score (mae): 0.407907120834863

--------------------------------------------------

Last transformer tried:

[('DeseasonTransform', {'m': 52, 'model': 'add'})]

Score (mae): 0.04226554848615107

--------------------------------------------------

Last transformer tried:

[('DeseasonTransform', {'m': 52, 'model': 'add'}), ('Transform', <function find_optimal_transformation.<locals>.boxcox_tr at 0x7fcff088d040>, {'lmbda': -0.5})]

Score (mae): 0.047544210787943963

--------------------------------------------------

Last transformer tried:

[('DeseasonTransform', {'m': 52, 'model': 'add'}), ('Transform', <function find_optimal_transformation.<locals>.boxcox_tr at 0x7fcff088d040>, {'lmbda': 0})]

Score (mae): 0.04573807786929981

--------------------------------------------------

Last transformer tried:

[('DeseasonTransform', {'m': 52, 'model': 'add'}), ('Transform', <function find_optimal_transformation.<locals>.boxcox_tr at 0x7fcff088d040>, {'lmbda': 0.5})]

Score (mae): 0.04392809054109548

--------------------------------------------------

Last transformer tried:

[('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 1)]

Score (mae): 0.08609820028223651

--------------------------------------------------

Last transformer tried:

[('DeseasonTransform', {'m': 52, 'model': 'add'}), ('DiffTransform', 52)]

Score (mae): 0.05863628346364504

--------------------------------------------------

Last transformer tried:

[('DeseasonTransform', {'m': 52, 'model': 'add'}), ('ScaleTransform',)]

Score (mae): 0.038603715602285725

--------------------------------------------------

Last transformer tried:

[('DeseasonTransform', {'m': 52, 'model': 'add'}), ('MinMaxTransform',)]

Score (mae): 0.042265548486150994

--------------------------------------------------

Final Selection:

[('DeseasonTransform', {'m': 52, 'model': 'add'}), ('ScaleTransform',)]

[103]:

mvpipeline = MVPipeline(

steps = [

('Transform',[transformer_vol,transformer_price]),

('Add Xvars',[add_vars]*2),

('Forecast',mvforecaster),

('Revert',[reverter_vol,reverter_price]),

],

test_length = 20,

cis = True,

names = ['volume','price'],

)

fvol_aut, fprice_aut = mvpipeline.fit_predict(

fvol_aut,

fprice_aut,

models=[

'mlr',

'elasticnet',

'xgboost',

'lightgbm',

],

) # returns a tuple of Forecaster objects

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

[104]:

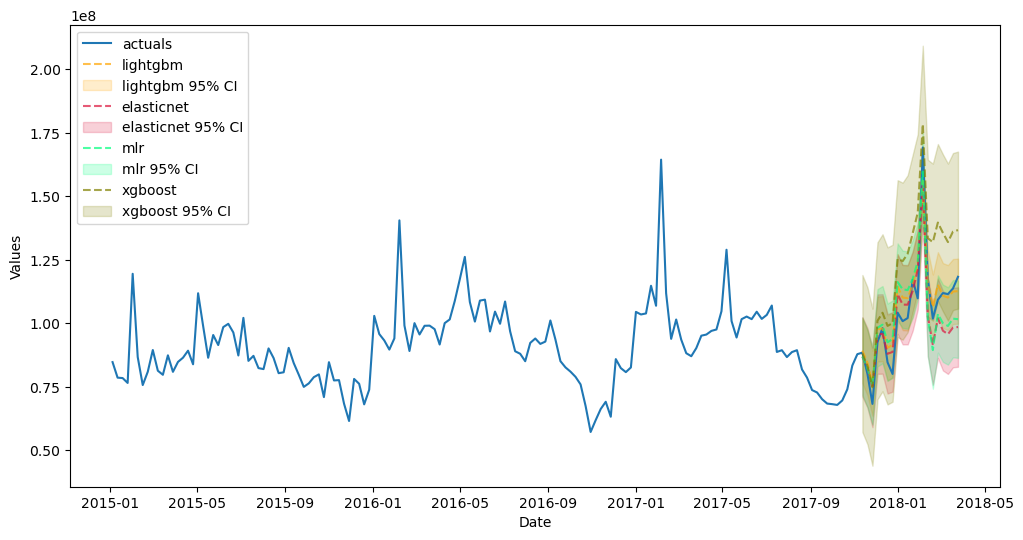

fvol_aut.plot_test_set(order_by='TestSetRMSE',ci=True)

plt.show()

[105]:

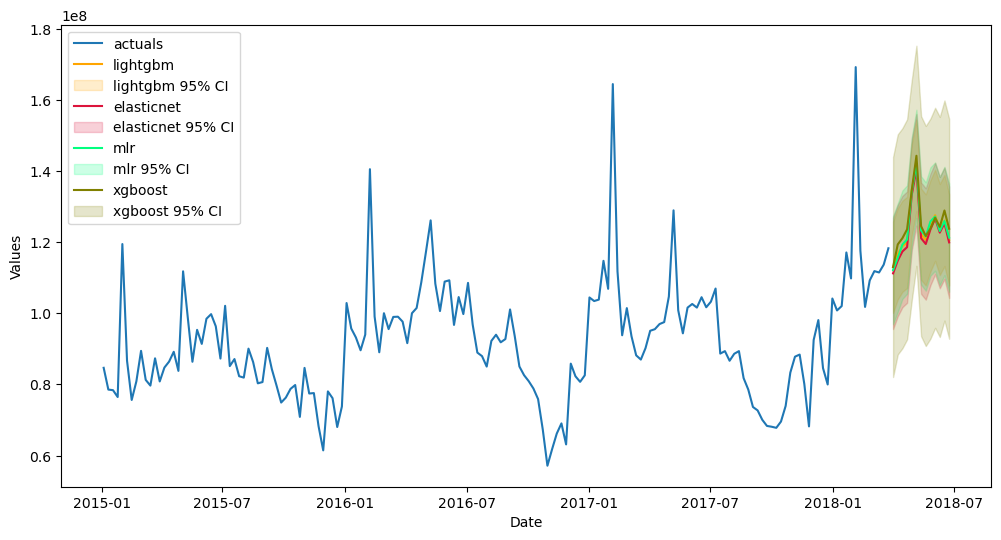

fvol_aut.plot(order_by='TestSetRMSE',ci=True)

plt.show()

Backtest Multivariate Pipeline

Like univariate pipelines, multivariate pipelines can also be backtested. Info about each model and series becomes possible to compare. See the documentation.

[106]:

# recreate Forecaster objects to bring dates back lost from taking seasonal differences

fvol_aut = Forecaster(

y=volume,

current_dates=volume.index,

future_dates=13,

)

fprice_aut = Forecaster(

y=price,

current_dates=price.index,

future_dates=13,

)

[107]:

mv_backtest_results = mvpipeline.backtest(

fvol_aut,

fprice_aut,

n_iter = 3,

jump_back = 13,

test_length = 0,

cis = False,

models=[

'mlr',

'elasticnet',

'xgboost',

'lightgbm',

],

)

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

[108]:

backtest_metrics(

mv_backtest_results,

mets=['smape','rmse','bias'],

names = ['Volume','Price'],

)

[108]:

| Iter0 | Iter1 | Iter2 | Average | |||

|---|---|---|---|---|---|---|

| Series | Model | Metric | ||||

| Volume | mlr | smape | 0.0544 | 0.1176 | 0.1582 | 0.1101 |

| rmse | 9,607,094.0997 | 10,760,756.5379 | 15,963,833.7533 | 12,110,561.4636 | ||

| bias | -69,742,732.2916 | -87,711,912.6597 | 157,394,405.8767 | -20,079.6915 | ||

| elasticnet | smape | 0.0662 | 0.1606 | 0.1398 | 0.1222 | |

| rmse | 10,759,298.7685 | 14,132,016.6443 | 14,134,913.2323 | 13,008,742.8817 | ||

| bias | -82,997,021.2184 | -139,537,507.0051 | 140,719,790.4827 | -27,271,579.2469 | ||

| xgboost | smape | 0.1315 | 0.1447 | 0.0713 | 0.1158 | |

| rmse | 20,090,059.9856 | 13,817,186.7925 | 7,510,114.4244 | 13,805,787.0675 | ||

| bias | 189,709,643.4190 | -129,669,530.7265 | 71,329,272.6822 | 43,789,795.1249 | ||

| lightgbm | smape | 0.1278 | 0.1161 | 0.1720 | 0.1386 | |

| rmse | 16,974,627.6371 | 10,539,060.5819 | 17,427,536.4398 | 14,980,408.2196 | ||

| bias | -182,115,273.5654 | -76,693,584.9027 | 184,015,627.3148 | -24,931,077.0511 | ||

| Price | mlr | smape | 0.0523 | 0.0762 | 0.0808 | 0.0698 |

| rmse | 0.0811 | 0.1307 | 0.1782 | 0.1300 | ||

| bias | 0.9321 | 1.0663 | -1.5867 | 0.1372 | ||

| elasticnet | smape | 0.0287 | 0.0606 | 0.1631 | 0.0841 | |

| rmse | 0.0461 | 0.1043 | 0.2838 | 0.1447 | ||

| bias | -0.1421 | 0.5670 | -3.3627 | -0.9793 | ||

| xgboost | smape | 0.0656 | 0.0513 | 0.1053 | 0.0740 | |

| rmse | 0.1000 | 0.1024 | 0.2100 | 0.1375 | ||

| bias | 1.1779 | 0.1599 | -2.2494 | -0.3038 | ||

| lightgbm | smape | 0.0287 | 0.0630 | 0.1588 | 0.0835 | |

| rmse | 0.0459 | 0.1215 | 0.2799 | 0.1491 | ||

| bias | -0.2103 | -0.1697 | -3.2847 | -1.2215 |

Through backtesting, we can see that the multivariate approach out-performed the univariate approach. Very cool!

Scaled Automated Forecasting

We can scale the fully automated approach to many series where we can then access all results through plotting with Jupyter widgets and export functions.

We produce a separate forecast for avocado sales in each region in our dataset.

This is done with a univariate approach, but cleverly using the code in this notebook, it could be transformed into a multivariate process where volume and price are forecasted together.

[109]:

from scalecast.notebook import results_vis

from tqdm.notebook import tqdm

[110]:

def forecaster_scaled(f,models):

f.auto_Xvar_select(

estimator='elasticnet',

monitor='TestSetMAE',

alpha=0.2,

irr_cycles = [26],

)

f.tune_test_forecast(

models,

dynamic_testing=13,

)

f.set_estimator('combo')

f.manual_forecast()

[111]:

results_dict = {}

for region in tqdm(data.region.unique()):

series = data.loc[data['region'] == region].groupby('Date')['Total Volume'].sum()

f_i = Forecaster(

y = series,

current_dates = series.index,

future_dates = 13,

test_length = .15,

validation_length = 13,

cis = True,

)

transformer_i, reverter_i = find_optimal_transformation(

f_i,

lags = 13,

m = 52,

monitor = 'mae',

estimator = 'elasticnet',

alpha = 0.2,

test_length = 13,

)

pipeline_i = Pipeline(

steps = [

('Transform',transformer_i),

('Forecast',forecaster_scaled),

('Revert',reverter_i),

]

)

f_i = pipeline_i.fit_predict(

f_i,

models=[

'mlr',

'elasticnet',

'xgboost',

'lightgbm',

'knn',

],

)

results_dict[region] = f_i

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 10 iterations

Finished loading model, total used 10 iterations

Finished loading model, total used 10 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 200 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 100 iterations

Finished loading model, total used 100 iterations

Finished loading model, total used 100 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Finished loading model, total used 250 iterations

Run the next two functions locally to see the full functionality of these widgets.

[112]:

results_vis(results_dict,'test')

[113]:

results_vis(results_dict)

Exporting Results

[114]:

from scalecast.multiseries import export_model_summaries

Exporting Results from a Single Forecaster Object

[115]:

results = f.export(cis=True,models=['mlr','lasso','ridge'])

results.keys()

[115]:

dict_keys(['model_summaries', 'lvl_fcsts', 'lvl_test_set_predictions'])

[116]:

for k, df in results.items():

print(f'{k} has these columns:',*df.columns,'-'*25,sep='\n')

model_summaries has these columns:

ModelNickname

Estimator

Xvars

HyperParams

Observations

DynamicallyTested

TestSetLength

CILevel

ValidationMetric

ValidationMetricValue

models

weights

best_model

InSampleRMSE

InSampleMAPE

InSampleMAE

InSampleR2

TestSetRMSE

TestSetMAPE

TestSetMAE

TestSetR2

-------------------------

lvl_fcsts has these columns:

DATE

mlr

mlr_upperci

mlr_lowerci

lasso

lasso_upperci

lasso_lowerci

ridge

ridge_upperci

ridge_lowerci

-------------------------

lvl_test_set_predictions has these columns:

DATE

actual

mlr

mlr_upperci

mlr_lowerci

lasso

lasso_upperci

lasso_lowerci

ridge

ridge_upperci

ridge_lowerci

-------------------------

[117]:

results['model_summaries'][['ModelNickname','HyperParams','TestSetRMSE','InSampleRMSE']]

[117]:

| ModelNickname | HyperParams | TestSetRMSE | InSampleRMSE | |

|---|---|---|---|---|

| 0 | mlr | {} | 16,818,489.5277 | 10,231,495.9303 |

| 1 | lasso | {'alpha': 0.2} | 16,818,489.9828 | 10,231,495.9303 |

| 2 | ridge | {'alpha': 0.2} | 16,827,165.4875 | 10,265,352.0145 |

Exporting Results from a Single MVForecaster Object

[118]:

mvresults = mvf.export(cis=True,models=['elasticnet','xgboost'])

mvresults.keys()

[118]:

dict_keys(['model_summaries', 'lvl_fcsts', 'lvl_test_set_predictions'])

[119]:

for k, df in mvresults.items():

print(f'{k} has these columns:',*df.columns,'-'*25,sep='\n')

model_summaries has these columns:

Series

ModelNickname

Estimator

Xvars

HyperParams

Lags

Observations

DynamicallyTested

TestSetLength

ValidationMetric

ValidationMetricValue

OptimizedOn

MetricOptimized

best_model

InSampleRMSE

InSampleMAPE

InSampleMAE

InSampleR2

TestSetRMSE

TestSetMAPE

TestSetMAE

TestSetR2

-------------------------

lvl_fcsts has these columns:

DATE

volume_elasticnet_lvl_fcst

volume_elasticnet_lvl_fcst_upper

volume_elasticnet_lvl_fcst_lower

volume_xgboost_lvl_fcst

volume_xgboost_lvl_fcst_upper

volume_xgboost_lvl_fcst_lower

price_elasticnet_lvl_fcst

price_elasticnet_lvl_fcst_upper

price_elasticnet_lvl_fcst_lower

price_xgboost_lvl_fcst

price_xgboost_lvl_fcst_upper

price_xgboost_lvl_fcst_lower

-------------------------

lvl_test_set_predictions has these columns:

DATE

volume_actuals

volume_elasticnet_lvl_ts

volume_elasticnet_lvl_ts_upper

volume_elasticnet_lvl_ts_lower

volume_xgboost_lvl_ts

volume_xgboost_lvl_ts_upper

volume_xgboost_lvl_ts_lower

price_actuals

price_elasticnet_lvl_ts

price_elasticnet_lvl_ts_upper

price_elasticnet_lvl_ts_lower

price_xgboost_lvl_ts

price_xgboost_lvl_ts_upper

price_xgboost_lvl_ts_lower

-------------------------

[120]:

mvresults['model_summaries'][['Series','ModelNickname','HyperParams','Lags','TestSetRMSE','InSampleRMSE']]

[120]:

| Series | ModelNickname | HyperParams | Lags | TestSetRMSE | InSampleRMSE | |

|---|---|---|---|---|---|---|

| 0 | volume | elasticnet | {'alpha': 0.2} | 13 | 18,694,896.5159 | 11,976,031.0554 |

| 1 | volume | xgboost | {'gamma': 1} | 13 | 22,606,056.1177 | 341.6022 |

| 2 | price | elasticnet | {'alpha': 0.2} | 13 | 0.1522 | 0.1561 |

| 3 | price | xgboost | {'gamma': 1} | 13 | 0.1292 | 0.1141 |

Exporting Results from a Dictionary of Forecaster Objects

[121]:

all_results = export_model_summaries(results_dict)

all_results[['ModelNickname','Series','Xvars','HyperParams','TestSetRMSE','InSampleRMSE']].sample(10)

[121]:

| ModelNickname | Series | Xvars | HyperParams | TestSetRMSE | InSampleRMSE | |

|---|---|---|---|---|---|---|

| 178 | knn | Northeast | [AR1, AR2, AR3, AR4, AR5, AR6, AR7, AR8, AR9, ... | {'n_neighbors': 54} | 724,041.5710 | 733,517.0246 |

| 17 | combo | BaltimoreWashington | None | {} | 154,661.0027 | 140,291.4529 |

| 56 | xgboost | CincinnatiDayton | [AR1, AR2, AR3, AR4, AR5, AR6, AR7, AR8, AR9, ... | {'n_estimators': 200, 'scale_pos_weight': 5, '... | 29,716.4527 | 7,782.8633 |

| 309 | lightgbm | TotalUS | [weeksin, weekcos, monthsin, monthcos, AR1, AR... | {'n_estimators': 250, 'boosting_type': 'dart',... | 8,587,458.9970 | 15,516,549.5493 |

| 115 | elasticnet | Indianapolis | [t, AR1, AR2, AR3, AR4, AR5, AR6, AR7, AR8, AR... | {'alpha': 2.0, 'l1_ratio': 0, 'normalizer': 'm... | 61,612.3263 | 37,420.2720 |

| 132 | mlr | LosAngeles | [weeksin, weekcos, monthsin, monthcos, quarter... | {'normalizer': 'scale'} | 538,249.2891 | 450,855.7099 |

| 23 | combo | Boise | None | {} | 12,828.5334 | 8,090.6574 |

| 141 | lightgbm | Louisville | [weeksin, weekcos, monthsin, monthcos, AR1, AR... | {'n_estimators': 150, 'boosting_type': 'dart',... | 17,403.8036 | 22,637.4852 |

| 290 | xgboost | StLouis | [AR1, AR2, AR3, AR4, AR5, AR6, AR7, AR8, AR9, ... | {'n_estimators': 250, 'scale_pos_weight': 5, '... | 44,612.6516 | 87.0324 |

| 112 | knn | Houston | [lnt, weeksin, weekcos, monthsin, monthcos, AR... | {'n_neighbors': 69} | 298,081.3679 | 250,425.0721 |

[ ]: