Transfer Learning

This notebook shows how to use one fitted model stored in a

Forecasterobject to make predictions on a separate time series.Requires

>=0.19.0As of

0.19.1, univariate sklearn and tensorflow (RNN/LSTM) models are supported for this type of process. Multivariate sklearn, then the rest of the model types will be worked on next.See the documentation.

[1]:

from scalecast.Forecaster import Forecaster

from scalecast.util import infer_apply_Xvar_selection, find_optimal_transformation

from scalecast.Pipeline import Pipeline, Transformer, Reverter

from scalecast import GridGenerator

import pandas_datareader as pdr

import matplotlib.pyplot as plt

import pandas as pd

[2]:

GridGenerator.get_example_grids()

Initiate the First Forecaster Object

This series ends December, 2020.

[3]:

df = pdr.get_data_fred(

'HOUSTNSA',

start = '1959-01-01',

end = '2020-12-31',

)

df.tail()

[3]:

| HOUSTNSA | |

|---|---|

| DATE | |

| 2020-08-01 | 122.5 |

| 2020-09-01 | 126.3 |

| 2020-10-01 | 131.2 |

| 2020-11-01 | 117.8 |

| 2020-12-01 | 115.1 |

[4]:

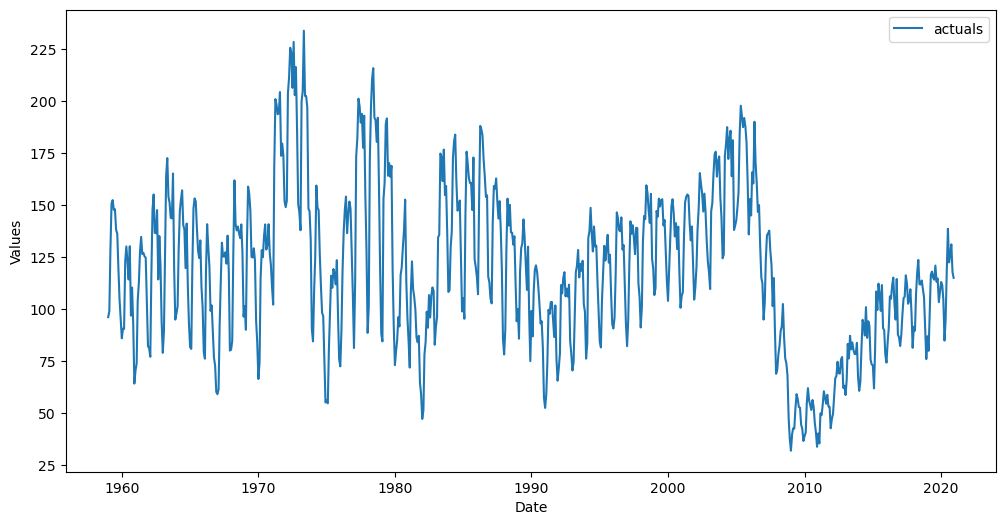

f = Forecaster(

y = df.iloc[:,0],

current_dates = df.index,

future_dates = 24,

)

f.plot()

plt.show()

Automatically add Xvars to the object

[5]:

f.auto_Xvar_select()

f

[5]:

Forecaster(

DateStartActuals=1959-01-01T00:00:00.000000000

DateEndActuals=2020-12-01T00:00:00.000000000

Freq=MS

N_actuals=744

ForecastLength=24

Xvars=['AR1', 'AR2', 'AR3', 'AR4']

TestLength=0

ValidationMetric=rmse

ForecastsEvaluated=[]

CILevel=None

CurrentEstimator=mlr

GridsFile=Grids

)

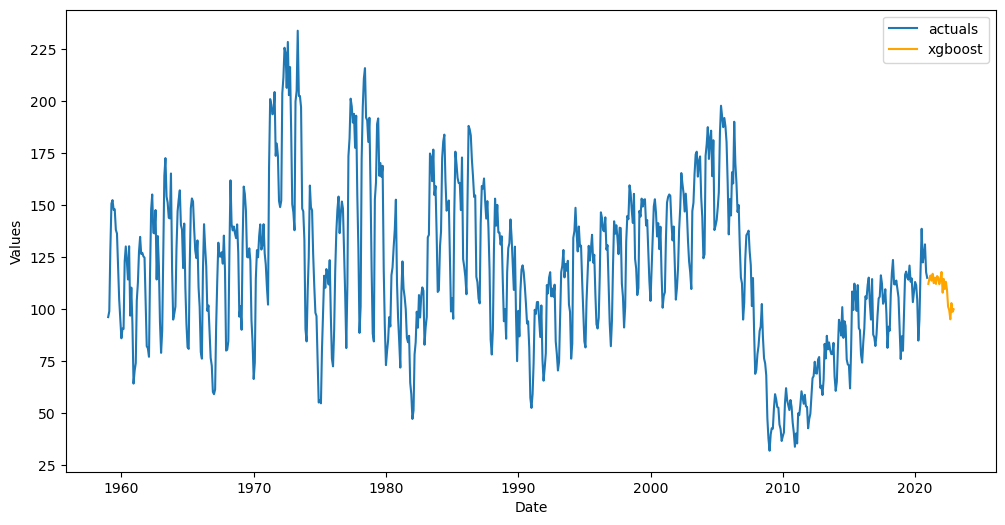

Fit an XGBoost Model and Make Predictions

[6]:

f.set_estimator('xgboost')

f.ingest_grid('xgboost')

f.limit_grid_size(10)

f.cross_validate(k=3,test_length=48)

f.auto_forecast()

View the Forecast

[7]:

f.plot()

plt.show()

Initiate the Second Forecaster Object

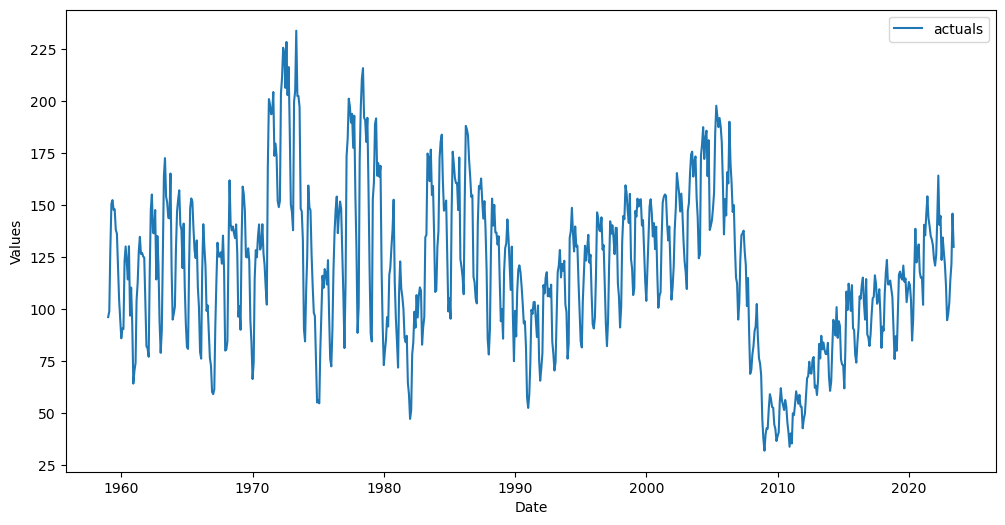

Later, if we have more data streaming in, instead of refitting a model, we can use the already-fitted model to make the predictions. This updated series is through June, 2023

You can use an updated version of the original series, you can use the same series with an extended Forecast horizon, or you can use an entirely different series (as long as it’s the same frequency) to perform this process

[8]:

df_new = pdr.get_data_fred(

'HOUSTNSA',

start = '1959-01-01',

end = '2023-06-30',

)

df_new.tail()

[8]:

| HOUSTNSA | |

|---|---|

| DATE | |

| 2023-02-01 | 103.2 |

| 2023-03-01 | 114.0 |

| 2023-04-01 | 121.7 |

| 2023-05-01 | 146.0 |

| 2023-06-01 | 130.0 |

[9]:

f_new = Forecaster(

y = df_new.iloc[:,0],

current_dates = df_new.index,

future_dates = 48,

)

f_new.plot()

plt.show()

Add the same Xvars to the new Forecaster object

The helper function below can assist when you automatically added Xvars

If you manually added Xvars, you can wrap the selection process in a function and run this new

Forecasterobject through the same function.

[10]:

f_new = infer_apply_Xvar_selection(infer_from=f,apply_to=f_new)

f_new

[10]:

Forecaster(

DateStartActuals=1959-01-01T00:00:00.000000000

DateEndActuals=2023-06-01T00:00:00.000000000

Freq=MS

N_actuals=774

ForecastLength=48

Xvars=['AR1', 'AR2', 'AR3', 'AR4']

TestLength=0

ValidationMetric=rmse

ForecastsEvaluated=[]

CILevel=None

CurrentEstimator=mlr

GridsFile=Grids

)

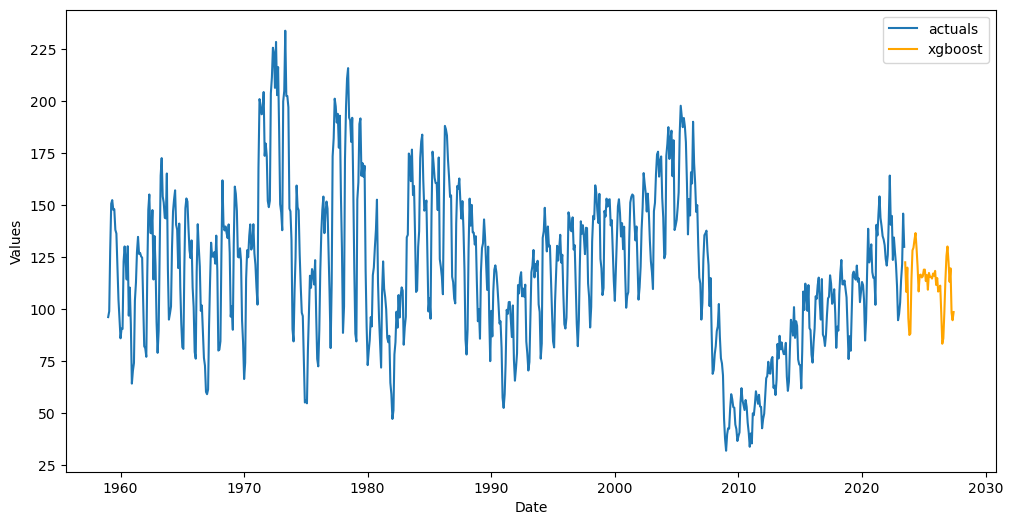

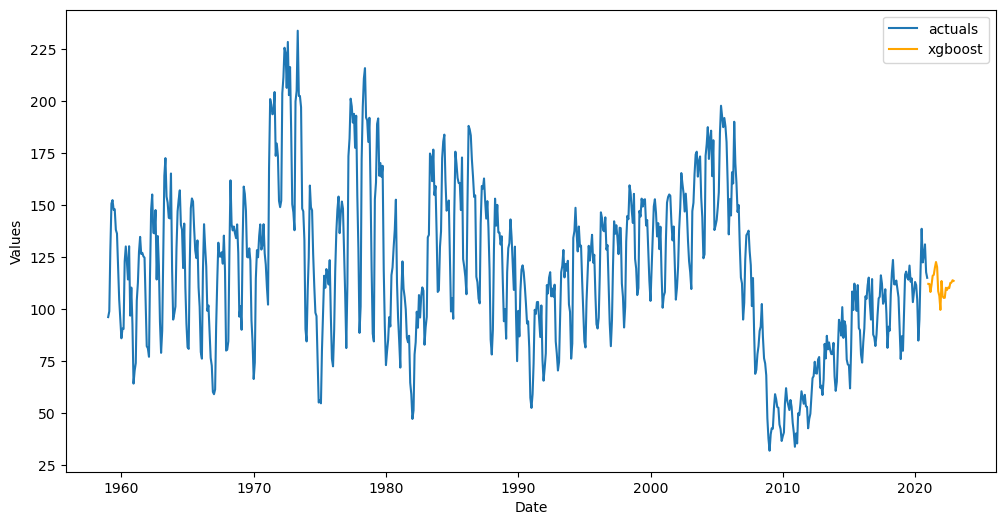

Apply fitted model from first object onto this new object

[11]:

f_new.transfer_predict(transfer_from=f,model='xgboost')

View the new forecast

[13]:

f_new.plot()

plt.show()

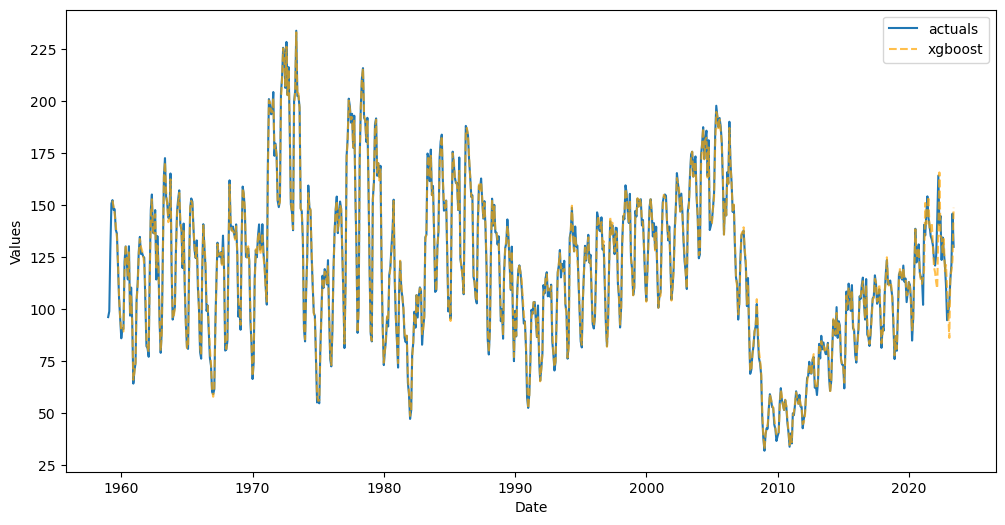

View the in-sample predictions

[14]:

f_new.plot_fitted()

plt.show()

In the below plot, the model has seen all observations until December, 2020. From January, 2021 through June, 2023, it is seeing those observations for the first time, but because it has the actual y observations, its predictions are expected to be more accurate than the forecast into the unknown horizon.

Predict over a specific date range

Instead of storing the model info into the new

Forecasterobject, you can instead get predicted output over a specific date range.

[15]:

preds = f_new.transfer_predict(

transfer_from = f,

model = 'xgboost',

dates = pd.date_range(start='2021-01-01',end='2023-12-31',freq='MS'),

save_to_history=False,

return_series=True,

)

preds

[15]:

2021-01-01 112.175186

2021-02-01 115.029518

2021-03-01 118.659706

2021-04-01 151.111618

2021-05-01 140.886765

2021-06-01 147.894882

2021-07-01 154.100571

2021-08-01 137.926544

2021-09-01 137.189224

2021-10-01 141.547058

2021-11-01 130.737900

2021-12-01 120.278030

2022-01-01 117.764030

2022-02-01 112.886353

2022-03-01 110.008720

2022-04-01 139.413696

2022-05-01 165.805817

2022-06-01 135.017914

2022-07-01 134.379486

2022-08-01 126.559814

2022-09-01 133.788025

2022-10-01 118.278656

2022-11-01 121.269691

2022-12-01 110.270599

2023-01-01 98.168579

2023-02-01 86.210205

2023-03-01 115.844292

2023-04-01 118.449600

2023-05-01 123.620918

2023-06-01 148.793396

2023-07-01 122.571846

2023-08-01 108.331818

2023-09-01 120.023163

2023-10-01 95.729309

2023-11-01 87.593613

2023-12-01 88.265671

dtype: float32

From January through June, 2021, the predictions are considered in-sample, although the model has never previously seen them (it predicted using the actual y observations over that timespan, and that is a form of leakage for auto-regressive time series models). The rest of the predictions are truly out-of-sample.

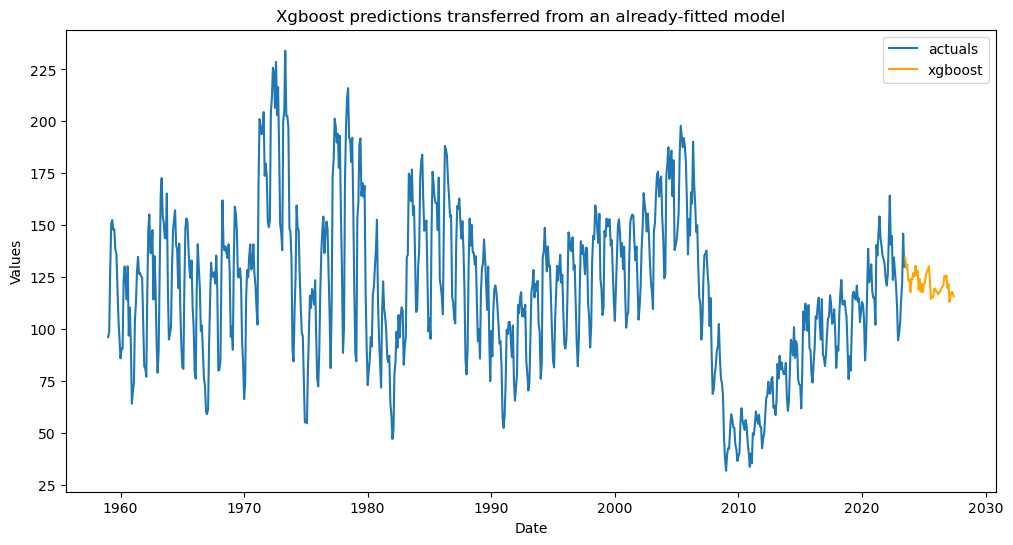

Transfer Predict in a Pipeline

We can use auto-transformation selection and pipelines to apply predictions from a fitted model into a new Forecaster object. This can be good to apply when new data frequently comes through and you don’t want to refit models.

Find optimal set of transformations

[16]:

transformer, reverter = find_optimal_transformation(f,verbose=True)

Using xgboost model to find the best transformation set on 1 test sets, each 24 in length.

All transformation tries will be evaluated with 12 lags.

Last transformer tried:

[]

Score (rmse): 19.44337760778588

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'loess': True})]

Score (rmse): 16.47704226214548

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 1})]

Score (rmse): 27.038328952689234

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 2})]

Score (rmse): 14.152673765108048

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 2}), ('DeseasonTransform', {'m': 12, 'model': 'add'})]

Score (rmse): 20.14955556372946

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 2}), ('DiffTransform', 1)]

Score (rmse): 18.150826589832704

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 2}), ('DiffTransform', 12)]

Score (rmse): 31.59079798104221

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 2}), ('ScaleTransform',)]

Score (rmse): 17.27265247612732

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 2}), ('MinMaxTransform',)]

Score (rmse): 13.685311300863027

--------------------------------------------------

Last transformer tried:

[('DetrendTransform', {'poly_order': 2}), ('RobustScaleTransform',)]

Score (rmse): 14.963448554311212

--------------------------------------------------

Final Selection:

[('DetrendTransform', {'poly_order': 2}), ('MinMaxTransform',)]

Fit the first pipeline

[17]:

def forecaster(f):

f.auto_Xvar_select()

f.ingest_grid('xgboost')

f.limit_grid_size(10)

f.cross_validate(k=3,test_length=48)

f.auto_forecast()

[18]:

pipeline = Pipeline(

steps = [

('Transform',transformer),

('Forecast',forecaster),

('Revert',reverter),

]

)

f = pipeline.fit_predict(f)

[19]:

f.plot()

plt.show()

Predict new data

[20]:

def transfer_forecast(f,transfer_from):

infer_apply_Xvar_selection(infer_from=transfer_from,apply_to=f)

f.transfer_predict(transfer_from=transfer_from,model='xgboost')

[21]:

pipeline_new = Pipeline(

steps = [

('Transform',transformer),

('Transfer Forecast',transfer_forecast),

('Revert',reverter),

]

)

f_new = pipeline_new.fit_predict(f_new,transfer_from=f) # even though it says fit, no model actually gets fit in the pipeline

[23]:

f_new.plot()

plt.title('Xgboost predictions transferred from an already-fitted model')

plt.show()

[ ]: