VECM

Using a VECM to predict FANG stocks

See the VECM documentation

[1]:

import pandas as pd

import numpy as np

from pandas_datareader import data as pdr

import yfinance as yf

from scalecast.Forecaster import Forecaster

from scalecast.MVForecaster import MVForecaster

from scalecast.Pipeline import Transformer, Reverter, MVPipeline

from scalecast.util import (

find_optimal_lag_order,

find_optimal_coint_rank,

Forecaster_with_missing_vals,

)

from scalecast.auxmodels import vecm

from scalecast.multiseries import export_model_summaries

from scalecast import GridGenerator

import matplotlib.pyplot as plt

[2]:

yf.pdr_override()

Download data using a public API

[3]:

FANG = [

'META',

'AMZN',

'NFLX',

'GOOG',

]

fs = []

for sym in FANG:

df = pdr.get_data_yahoo(sym)

# since the api doesn't send the data exactly in Business-day frequency

# we can correct it using this function

f = Forecaster_with_missing_vals(

y=df['Close'],

current_dates = df.index,

future_dates = 65,

end = '2022-09-30',

desired_frequency = 'B',

fill_strategy = 'linear_interp',

add_noise = True,

noise_lookback = 5,

)

fs.append(f)

mvf = MVForecaster(*fs,names=FANG,test_length=65)

mvf.set_validation_metric('rmse')

mvf.add_sklearn_estimator(vecm,'vecm')

mvf

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

[3]:

MVForecaster(

DateStartActuals=2012-05-18T00:00:00.000000000

DateEndActuals=2023-08-03T00:00:00.000000000

Freq=B

N_actuals=2925

N_series=4

SeriesNames=['META', 'AMZN', 'NFLX', 'GOOG']

ForecastLength=65

Xvars=[]

TestLength=65

ValidationLength=1

ValidationMetric=rmse

ForecastsEvaluated=[]

CILevel=None

CurrentEstimator=mlr

OptimizeOn=mean

GridsFile=MVGrids

)

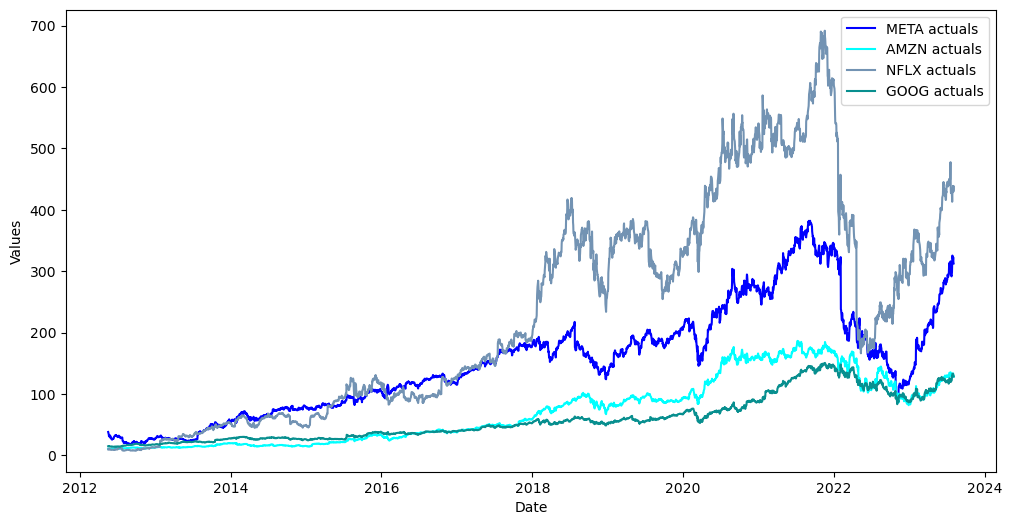

[4]:

mvf.plot()

plt.show()

Augmented Dickey Fuller Tests to Confirm Unit-1 Roots

[5]:

for stock, f in zip(FANG,fs):

adf_result = f.adf_test(full_res=True)

print('the stock {} is {}stationary at level'.format(

stock,

'not ' if adf_result[1] > 0.05 else ''

)

)

the stock META is not stationary at level

the stock AMZN is not stationary at level

the stock NFLX is not stationary at level

the stock GOOG is not stationary at level

[6]:

for stock, f in zip(FANG,fs):

adf_result = f.adf_test(diffy=True,full_res=True)

print('the stock {} is {}stationary at its first difference'.format(

stock,

'not ' if adf_result[1] > 0.05 else ''

)

)

the stock META is stationary at its first difference

the stock AMZN is stationary at its first difference

the stock NFLX is stationary at its first difference

the stock GOOG is stationary at its first difference

Measure IC to Find Optimal Lag Order

this is used to run the cointegration test

[7]:

lag_test = find_optimal_lag_order(mvf,train_only=True)

pd.DataFrame(

{

'aic':lag_test.aic,

'bic':lag_test.bic,

'hqic':lag_test.hqic,

'fpe':lag_test.fpe,

},

index = ['optimal lag order'],

).T

[7]:

| optimal lag order | |

|---|---|

| aic | 27 |

| bic | 1 |

| hqic | 3 |

| fpe | 27 |

Johansen cointegration test

[8]:

coint_res = find_optimal_coint_rank(

mvf,

det_order=1,

k_ar_diff=10,

train_only=True,

)

print(coint_res)

coint_res.rank

Johansen cointegration test using trace test statistic with 5% significance level

=====================================

r_0 r_1 test statistic critical value

-------------------------------------

0 4 56.60 55.25

1 4 33.50 35.01

-------------------------------------

[8]:

1

We found a cointegration rank of 1.

Run VECM

Now, we can specify a grid that will try more lags, deterministic terms, seasonal fluctuations, and cointegration ranks of 0 and 1

[9]:

vecm_grid = dict(

lags = [0], # required to set this to 0 for the vecm model in scalecast

freq = ['B'], # only necessary to suppress a warning

k_ar_diff = range(1,66), # lag orders to try

coint_rank = [0,1],

deterministic = ["n","co","lo","li","cili","colo"],

seasons = [0,5,30,65,260],

)

mvf.set_estimator('vecm')

mvf.ingest_grid(vecm_grid)

mvf.limit_grid_size(100,random_seed=20)

mvf.cross_validate(k=3,verbose=True)

mvf.auto_forecast()

results = mvf.export('model_summaries')

results[[

'ModelNickname',

'Series',

'TestSetRMSE',

'TestSetMAE',

]]

Num hyperparams to try for the vecm model: 100.

Fold 0: Train size: 2145 (2012-05-18 00:00:00 - 2020-08-06 00:00:00). Test Size: 715 (2020-08-07 00:00:00 - 2023-05-04 00:00:00).

Fold 1: Train size: 1430 (2012-05-18 00:00:00 - 2017-11-09 00:00:00). Test Size: 715 (2017-11-10 00:00:00 - 2020-08-06 00:00:00).

Fold 2: Train size: 715 (2012-05-18 00:00:00 - 2015-02-12 00:00:00). Test Size: 715 (2015-02-13 00:00:00 - 2017-11-09 00:00:00).

Chosen paramaters: {'lags': 0, 'freq': 'B', 'k_ar_diff': 28, 'coint_rank': 1, 'deterministic': 'li', 'seasons': 5}.

[9]:

| ModelNickname | Series | TestSetRMSE | TestSetMAE | |

|---|---|---|---|---|

| 0 | vecm | META | 50.913814 | 44.133838 |

| 1 | vecm | AMZN | 23.752750 | 22.348669 |

| 2 | vecm | NFLX | 113.705564 | 105.310047 |

| 3 | vecm | GOOG | 18.846431 | 18.041912 |

View VECM Results

[10]:

results['TestSetRMSE'].mean()

[10]:

51.80463965264752

[11]:

mvf.export_validation_grid('vecm').sample(15)

[11]:

| lags | freq | k_ar_diff | coint_rank | deterministic | seasons | Fold0Metric | Fold1Metric | Fold2Metric | AverageMetric | MetricEvaluated | Optimized On | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 71 | 0 | B | 58 | 0 | colo | 0 | 162.599874 | 44.268484 | 26.594518 | 77.820958 | rmse | mean |

| 40 | 0 | B | 7 | 0 | li | 260 | NaN | NaN | NaN | NaN | rmse | mean |

| 3 | 0 | B | 54 | 1 | lo | 30 | 110.553065 | 51.443275 | 19.154490 | 60.383610 | rmse | mean |

| 30 | 0 | B | 29 | 0 | co | 30 | 112.035140 | 44.427934 | 18.598329 | 58.353801 | rmse | mean |

| 76 | 0 | B | 1 | 1 | cili | 65 | 93.945660 | 51.090754 | 21.836356 | 55.624257 | rmse | mean |

| 87 | 0 | B | 50 | 0 | lo | 260 | 163.152289 | 46.616014 | 13.327631 | 74.365311 | rmse | mean |

| 10 | 0 | B | 44 | 0 | cili | 65 | NaN | NaN | NaN | NaN | rmse | mean |

| 9 | 0 | B | 47 | 0 | n | 0 | 86.212252 | 55.639330 | 36.182421 | 59.344668 | rmse | mean |

| 94 | 0 | B | 38 | 1 | colo | 5 | 139.580751 | 41.852200 | 24.055439 | 68.496130 | rmse | mean |

| 43 | 0 | B | 55 | 1 | colo | 260 | 112.237679 | 43.782141 | 63.595936 | 73.205252 | rmse | mean |

| 73 | 0 | B | 40 | 0 | lo | 0 | 159.422501 | 46.642590 | 18.090453 | 74.718515 | rmse | mean |

| 62 | 0 | B | 18 | 1 | n | 5 | 166.241648 | 54.618358 | 30.753820 | 83.871275 | rmse | mean |

| 63 | 0 | B | 12 | 0 | co | 260 | 108.180519 | 44.685347 | 23.286315 | 58.717394 | rmse | mean |

| 60 | 0 | B | 21 | 1 | li | 260 | 82.029398 | 50.186756 | 31.553748 | 54.589967 | rmse | mean |

| 64 | 0 | B | 43 | 1 | co | 0 | 100.291180 | 46.496187 | 16.839982 | 54.542450 | rmse | mean |

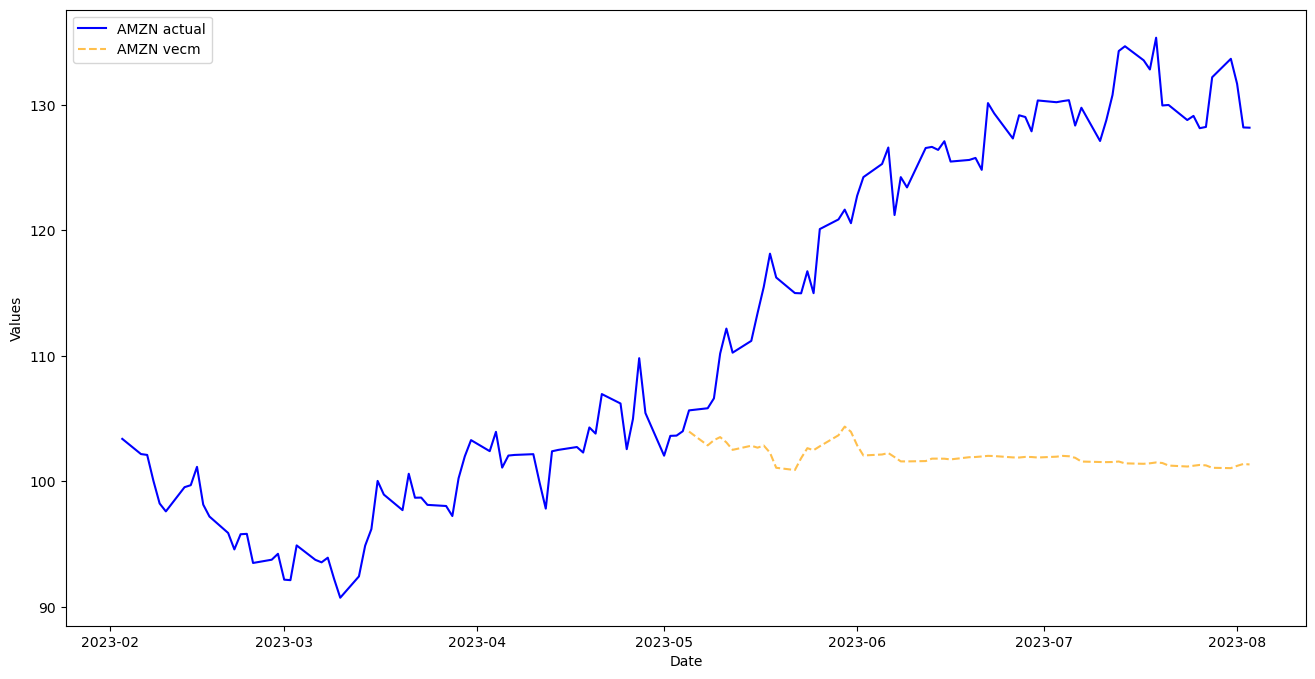

[12]:

mvf.plot_test_set(

series='AMZN',

models='vecm',

include_train=130,

figsize=(16,8)

)

plt.show()

Re-weight Evaluation Metrics and Rerun VECM

[13]:

weights = results['TestSetRMSE'] / results['TestSetRMSE'].sum()

weights

[13]:

0 0.245701

1 0.114627

2 0.548723

3 0.090950

Name: TestSetRMSE, dtype: float64

[14]:

mvf.set_optimize_on(

lambda x: (

x[0]*weights[0] +

x[1]*weights[1] +

x[2]*weights[2] +

x[3]*weights[3]

)

)

mvf.ingest_grid(vecm_grid)

mvf.limit_grid_size(100,random_seed=20)

mvf.cross_validate(k=3,verbose=True)

mvf.auto_forecast(call_me='vecm_weighted')

results = mvf.export('model_summaries')

results[[

'ModelNickname',

'Series',

'TestSetRMSE',

'TestSetMAE',

]]

Num hyperparams to try for the vecm model: 100.

Fold 0: Train size: 2145 (2012-05-18 00:00:00 - 2020-08-06 00:00:00). Test Size: 715 (2020-08-07 00:00:00 - 2023-05-04 00:00:00).

Fold 1: Train size: 1430 (2012-05-18 00:00:00 - 2017-11-09 00:00:00). Test Size: 715 (2017-11-10 00:00:00 - 2020-08-06 00:00:00).

Fold 2: Train size: 715 (2012-05-18 00:00:00 - 2015-02-12 00:00:00). Test Size: 715 (2015-02-13 00:00:00 - 2017-11-09 00:00:00).

Chosen paramaters: {'lags': 0, 'freq': 'B', 'k_ar_diff': 62, 'coint_rank': 1, 'deterministic': 'li', 'seasons': 0}.

[14]:

| ModelNickname | Series | TestSetRMSE | TestSetMAE | |

|---|---|---|---|---|

| 0 | vecm | META | 50.913814 | 44.133838 |

| 1 | vecm_weighted | META | 33.772797 | 28.520031 |

| 2 | vecm | AMZN | 23.752750 | 22.348669 |

| 3 | vecm_weighted | AMZN | 15.835426 | 14.617043 |

| 4 | vecm | NFLX | 113.705564 | 105.310047 |

| 5 | vecm_weighted | NFLX | 59.887563 | 53.210215 |

| 6 | vecm | GOOG | 18.846431 | 18.041912 |

| 7 | vecm_weighted | GOOG | 16.757831 | 16.121594 |

[15]:

results.loc[results['ModelNickname'] == 'vecm_weighted','TestSetRMSE'].mean()

[15]:

31.56340410699967

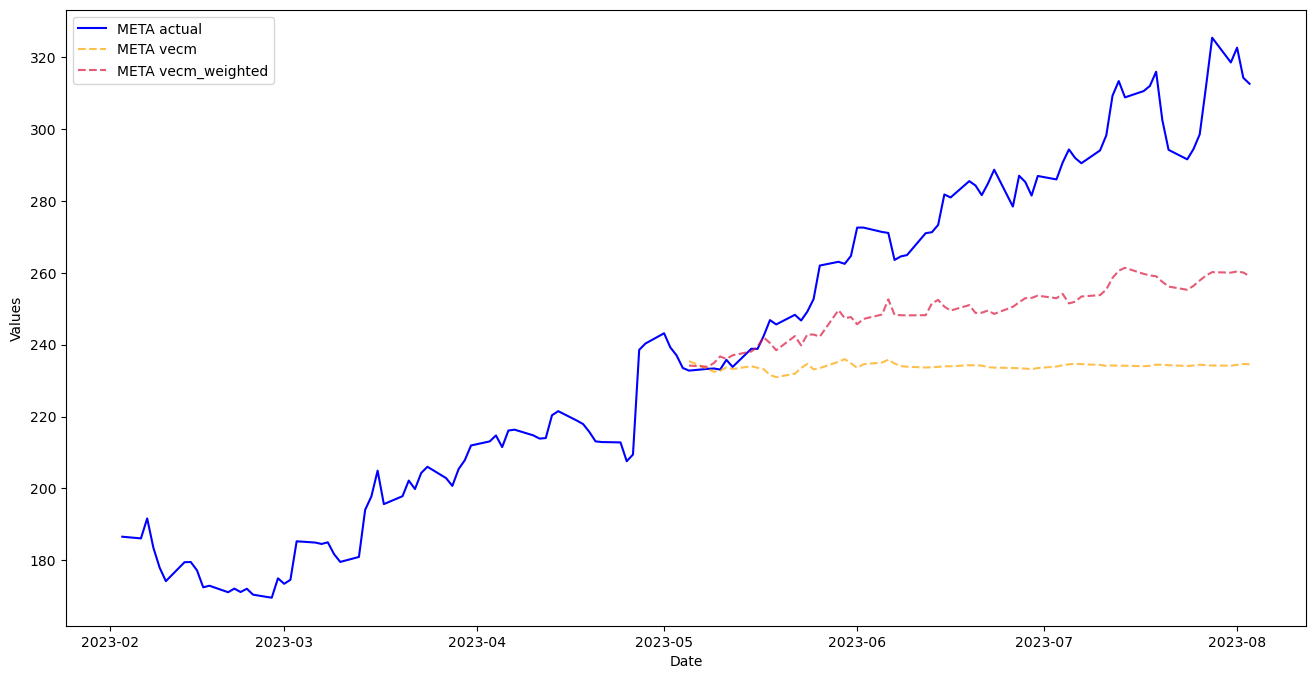

An improvement by weighting the optimizer!

[16]:

mvf.plot_test_set(

series='META',

models='all',

include_train=130,

figsize=(16,8)

)

plt.show()

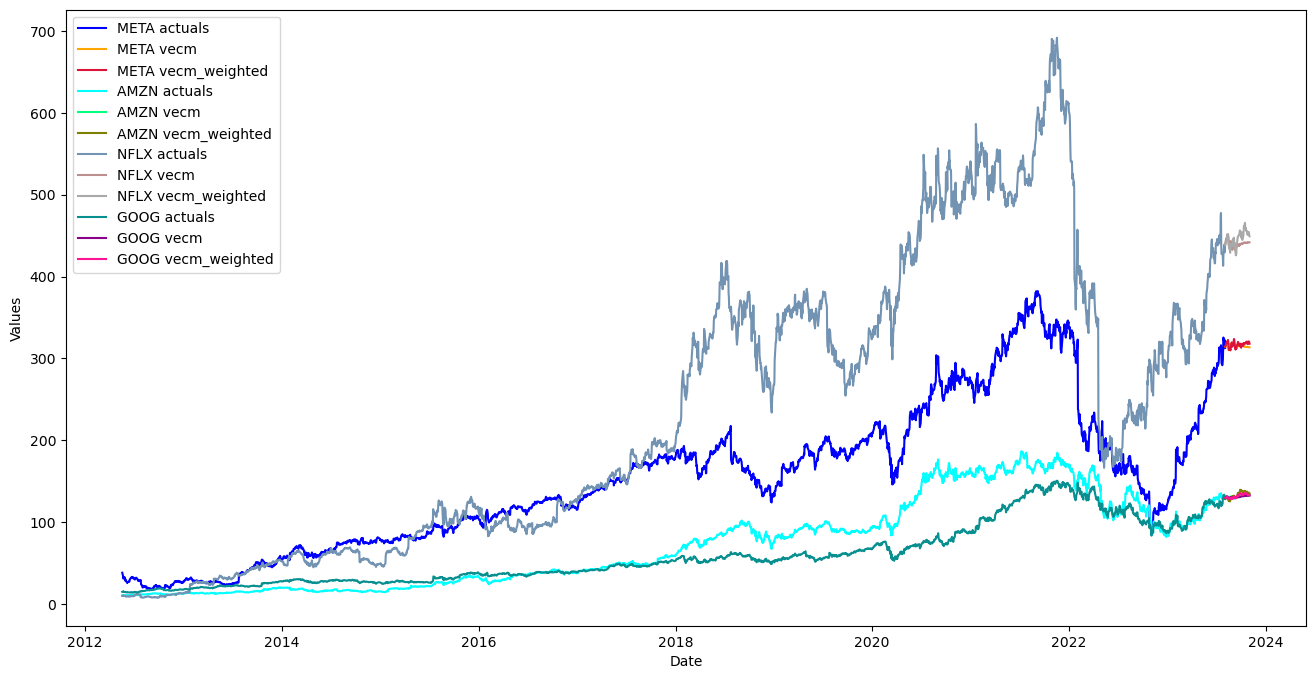

[17]:

mvf.plot(

series='all',

models='all',

figsize=(16,8)

)

plt.show()

Try Other MV Models

[31]:

GridGenerator.get_mv_grids()

# open MVGrids.py and manually change all lags arguments to range(1,66)

[32]:

transformers = []

reverters = []

for stock, f in zip(FANG,fs):

transformer = Transformer(

transformers = [('DiffTransform',)]

)

reverter = Reverter(

reverters = [('DiffRevert',)],

base_transformer = transformer,

)

transformers.append(transformer)

reverters.append(reverter)

[33]:

def Xvar_select(f):

f.set_validation_length(65)

f.auto_Xvar_select(

estimator='gbt',

max_depth=2,

max_ar=0, # in mv modeling, lags are a hyperparameter, not a regressor in the MVForecaster object

)

def mvforecaster(mvf):

models = (

'mlr',

'elasticnet',

'gbt',

'xgboost',

'lightgbm',

'knn',

)

mvf.set_test_length(65)

mvf.tune_test_forecast(

models,

limit_grid_size=10,

cross_validate=True,

k=3,

)

[34]:

pipeline = MVPipeline(

steps = [

('Transform',transformers),

('Xvar Select',[Xvar_select]*4),

('Forecast',mvforecaster),

('Revert',reverters),

],

names = FANG,

)

[35]:

fs = pipeline.fit_predict(*fs)

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

Finished loading model, total used 150 iterations

[36]:

results = export_model_summaries(dict(zip(FANG,fs)))

View Results

[37]:

model_rmses = results.groupby('ModelNickname')['TestSetRMSE'].mean().sort_values().reset_index()

model_rmses

[37]:

| ModelNickname | TestSetRMSE | |

|---|---|---|

| 0 | xgboost | 27.918698 |

| 1 | knn | 41.832711 |

| 2 | mlr | 42.519262 |

| 3 | gbt | 43.895070 |

| 4 | elasticnet | 44.320649 |

| 5 | lightgbm | 44.554279 |

The above table is the mean mape performance from each model over all series.

[38]:

series_rmses = results.groupby('Series')['TestSetRMSE'].min().reset_index()

series_rmses['Model'] = [

results.loc[

results['TestSetRMSE'] == i,

'ModelNickname'

].values[0] for i in series_rmses['TestSetRMSE']

]

series_rmses

[38]:

| Series | TestSetRMSE | Model | |

|---|---|---|---|

| 0 | AMZN | 17.433315 | xgboost |

| 1 | GOOG | 12.892690 | xgboost |

| 2 | META | 10.509525 | xgboost |

| 3 | NFLX | 70.839262 | xgboost |

[39]:

series_rmses['TestSetRMSE'].mean()

[39]:

27.918697955026953

The above table shows the best model for each series and its derived RMSE. The average RMSE of all these models applied to the individual series is 27.9, but being so dependent on the test set to choose the model probably leads to overfitting.

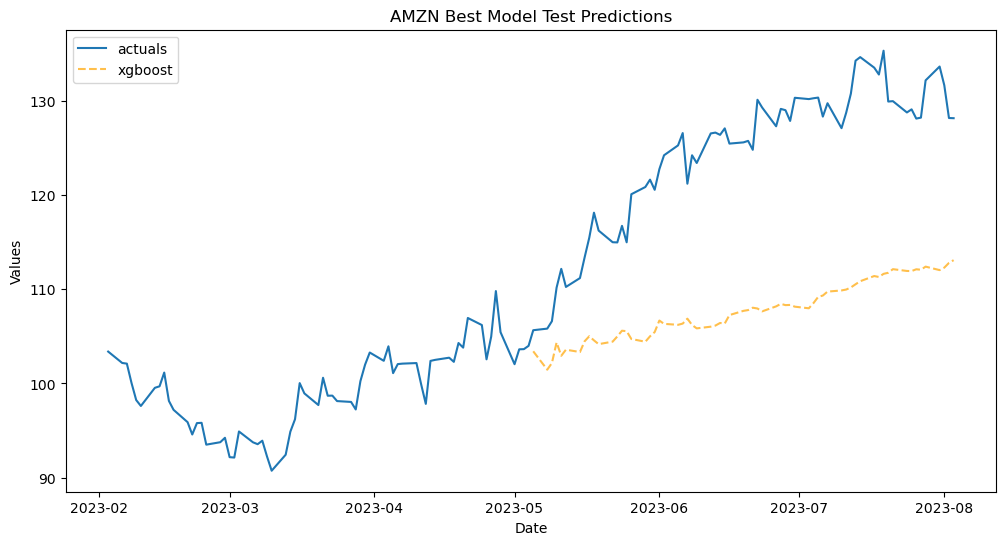

[41]:

fs[1].plot_test_set(

models='xgboost',

include_train=130,

)

plt.title('AMZN Best Model Test Predictions')

plt.show()

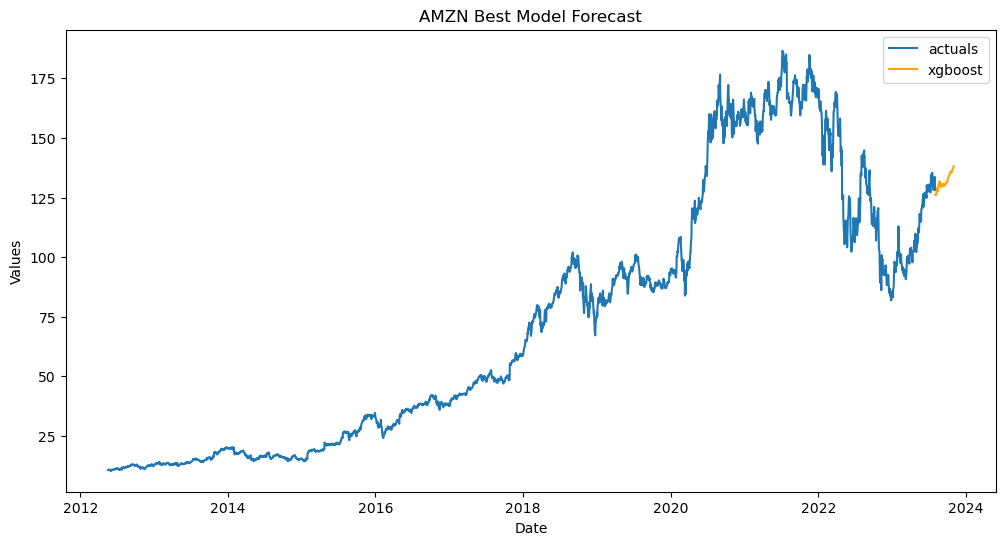

[42]:

fs[1].plot(

models='xgboost',

)

plt.title('AMZN Best Model Forecast')

plt.show()

[ ]: